The Monthly Natural Gas Market Newsletter - September 2022

FireSide Natural Gas Monthly Report - September 2022

Natural Gas Prices

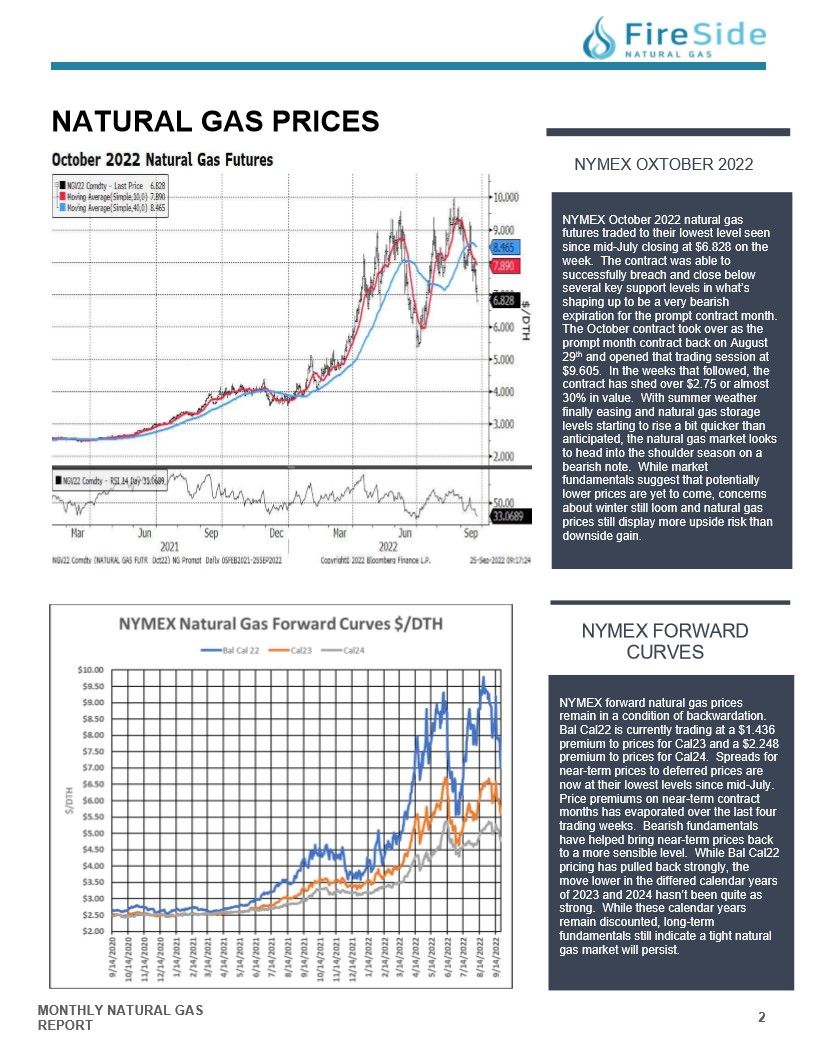

NYMEX OCTOBER 2022

NYMEX October 2022 natural gas futures traded to their lowest level seen since mid-July closing at $6.828 on the week. The contract was able to successfully breach and close below several key support levels in what's shaping up to be a very bearish expiration for the prompt contract month. The October contract took over as the prompt month contract back on August 29th and opened that trading session at $9.605. In the weeks that followed, the contract has shed over $2.75 or almost 30% in value. With summer weather finally easing and natural gas storage levels starting to rise a bit quicker than anticipated, the natural gas market looks to head into the shoulder season on a bearish note. While market fundamentals suggest that potentially lower prices are yet to come, concerns about winter still loom and natural gas prices still display more upside risk than downside gain.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of backwardation.

Bal Cal22 is currently trading at a $1.436

premium to prices for Cal23 and a $2.248

premium to prices for Cal24. Spreads for

near-term prices to deferred prices are

now at their lowest levels since mid-July.

Price premiums on near-term contract

months has evaporated over the last four

trading weeks. Bearish fundamentals

have helped bring near-term prices back

to a more sensible level. While Bal Cal22

pricing has pulled back strongly, the

move lower in the differed calendar years

of 2023 and 2024 hasn't been quite as

strong. While these calendar years

remain discounted, long-term

fundamentals still indicate a tight natural

gas market will persist.

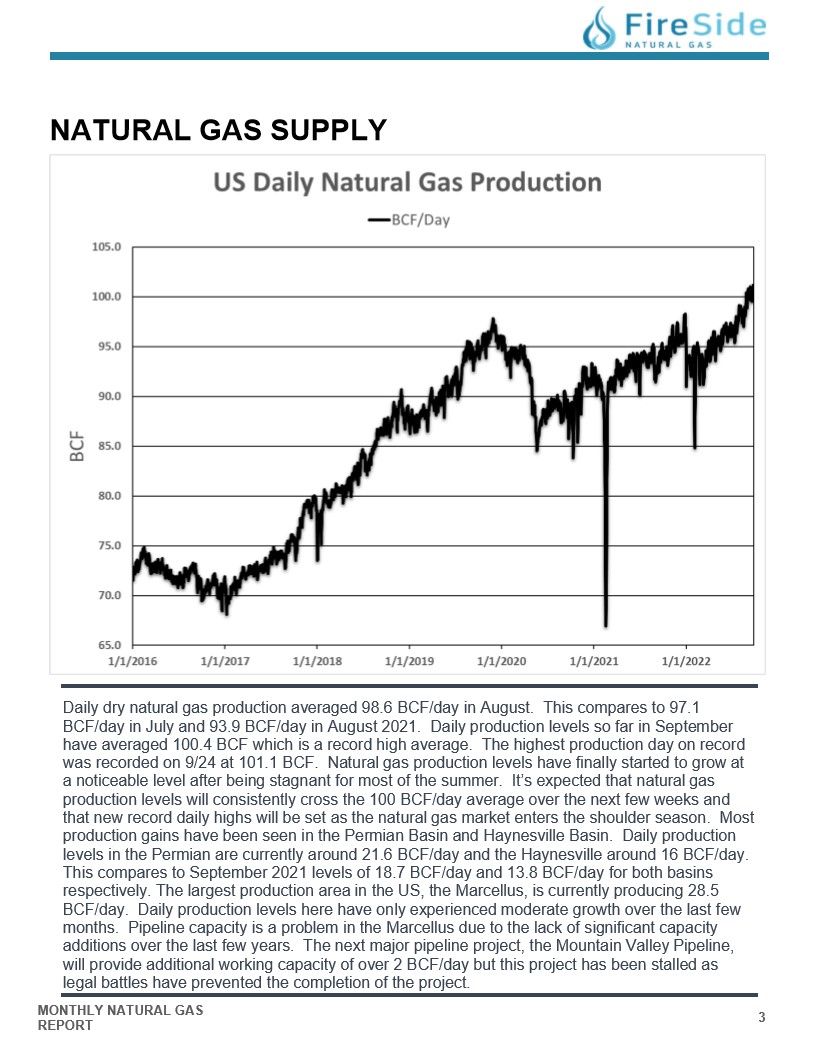

US DAILY NATURAL GAS PRODUCTION

Daily dry natural gas production averaged 98.6 BCF/day in August. This compares to 97.1 BCF/day in July and 93.9 BCF/day in August 2021. Daily production levels so far in September have averaged 100.4 BCF which is a record high average. The highest production day on record was recorded on 9/24 at 101.1 BCF. Natural gas production levels have finally started to grow at a noticeable level after being stagnant for most of the summer. It's expected that natural gas production levels will consistently cross the 100 BCF/day average over the next few weeks and that new record daily highs will be set as the natural gas market enters the shoulder season. Most production gains have been seen in the Permian Basin and Haynesville Basin. Daily production levels in the Permian are currently around 21.6 BCF/day and the Haynesville around 16 BCF/day. This compares to September 2021 levels of 18.7 BCF/day and 13.8 BCF/day for both basins respectively. The largest production area in the US, the Marcellus, is currently producing 28.5 BCF/day. Daily production levels here have only experienced moderate growth over the last few months. Pipeline capacity is a problem in the Marcellus due to the lack of significant capacity additions over the last few years. The next major pipeline project, the Mountain Valley Pipeline, will provide additional working capacity of over 2 BCF/day but this project has been stalled as legal battles have prevented the completion of the project.

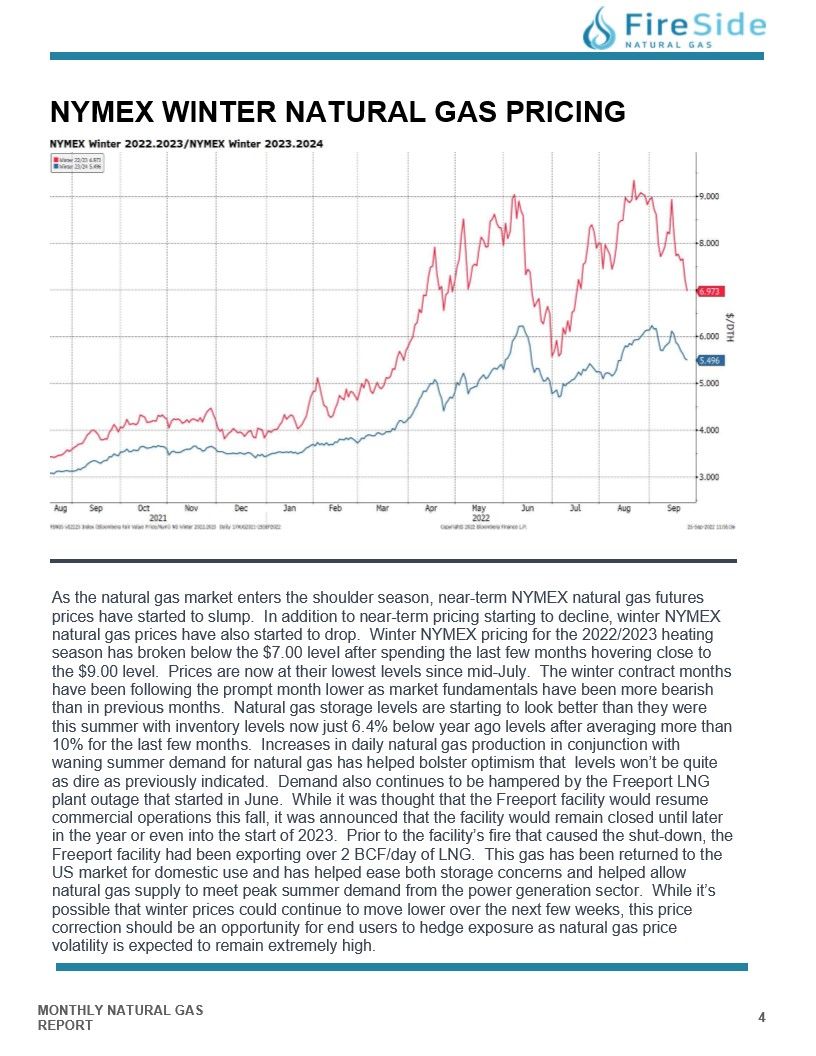

NYMEX WINTER NATURAL GAS PRICING

As the natural gas market enters the shoulder season, near-term NYMEX natural gas futures

prices have started to slump. In addition to near-term pricing starting to decline, winter NYMEX

natural gas prices have also started to drop. Winter NYMEX pricing for the 2022/2023 heating

season has broken below the $7.00 level after spending the last few months hovering close to

the $9.00 level. Prices are now at their lowest levels since mid-July. The winter contract months

have been following the prompt month lower as market fundamentals have been more bearish

than in previous months. Natural gas storage levels are starting to look better than they were

this summer with inventory levels now just 6.4% below year ago levels after averaging more than

10% for the last few months. Increases in daily natural gas production in conjunction with

waning summer demand for natural gas has helped bolster optimism that levels won't be quite

as dire as previously indicated. Demand also continues to be hampered by the Freeport LNG

plant outage that started in June. While it was thought that the Freeport facility would resume

commercial operations this fall, it was announced that the facility would remain closed until later

in the year or even into the start of 2023. Prior to the facility's fire that caused the shut-down, the

Freeport facility had been exporting over 2 BCF/day of LNG. This gas has been returned to the

US market for domestic use and has helped ease both storage concerns and helped allow

natural gas supply to meet peak summer demand from the power generation sector. While it's

possible that winter prices could continue to move lower over the next few weeks, this price

correction should be an opportunity for end users to hedge exposure as natural gas price

volatility is expected to remain extremely high.

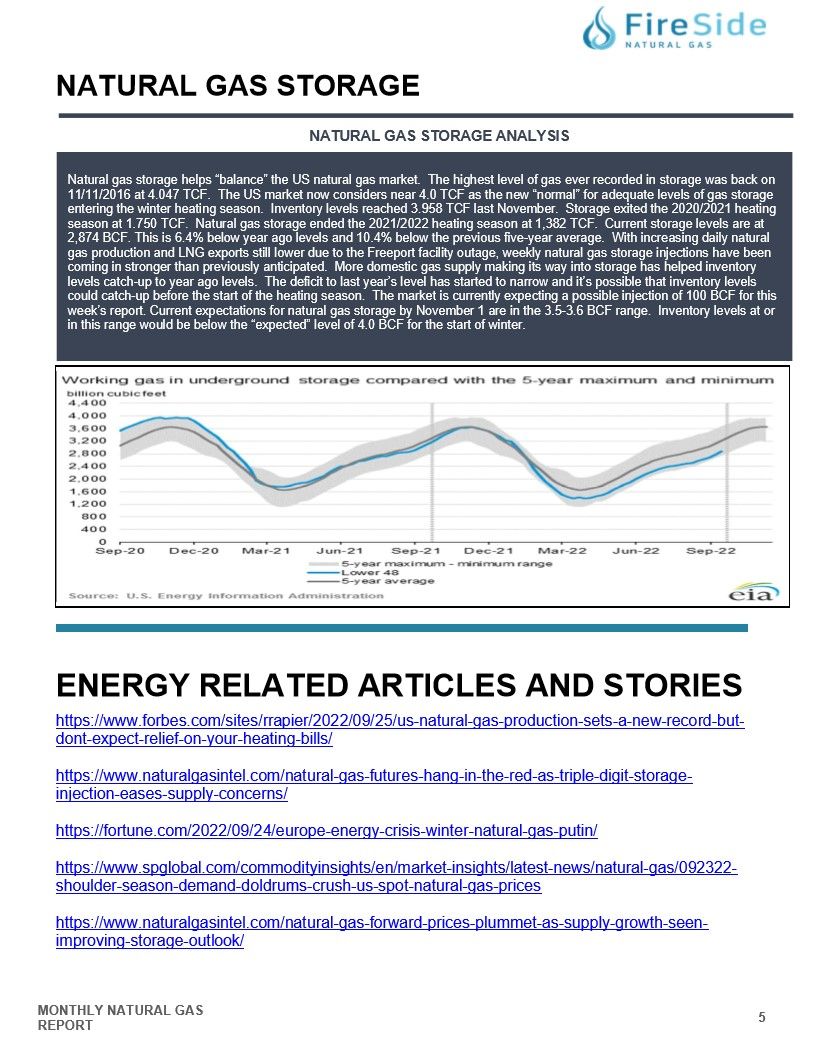

NATURAL GAS STORAGE ANALYSIS

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on 11/11/2016 at 4.047 TCF. The US market now considers near 4.0 TCF as the new "normal" for adequate levels of gas storage entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating season at 1.750 TCF. Natural gas storage ended the 2021/2022 heating season at 1,382 TCF. Current storage levels are at 2,874 BCF. This is 6.4% below year ago levels and 10.4% below the previous five-year average. With increasing daily natural gas production and LNG exports still lower due to the Freeport facility outage, weekly natural gas storage injections have been coming in stronger than previously anticipated. More domestic gas supply making its way into storage has helped inventory levels catch-up to year ago levels. The deficit to last year's level has started to narrow and it's possible that inventory levels could catch-up before the start of the heating season. The market is currently expecting a possible injection of 100 BCF for this week's report. Current expectations for natural gas storage by November 1 are in the 3.5-3.6 BCF range. Inventory levels at or in this range would be below the "expected" level of 4.0 BCF for the start of winter.

ENERGY RELATED ARTICLES AND STORIES