The Monthly Natural Gas Market Newsletter - October 2021

FireSide Natural Gas Monthly Report

Natural Gas Prices

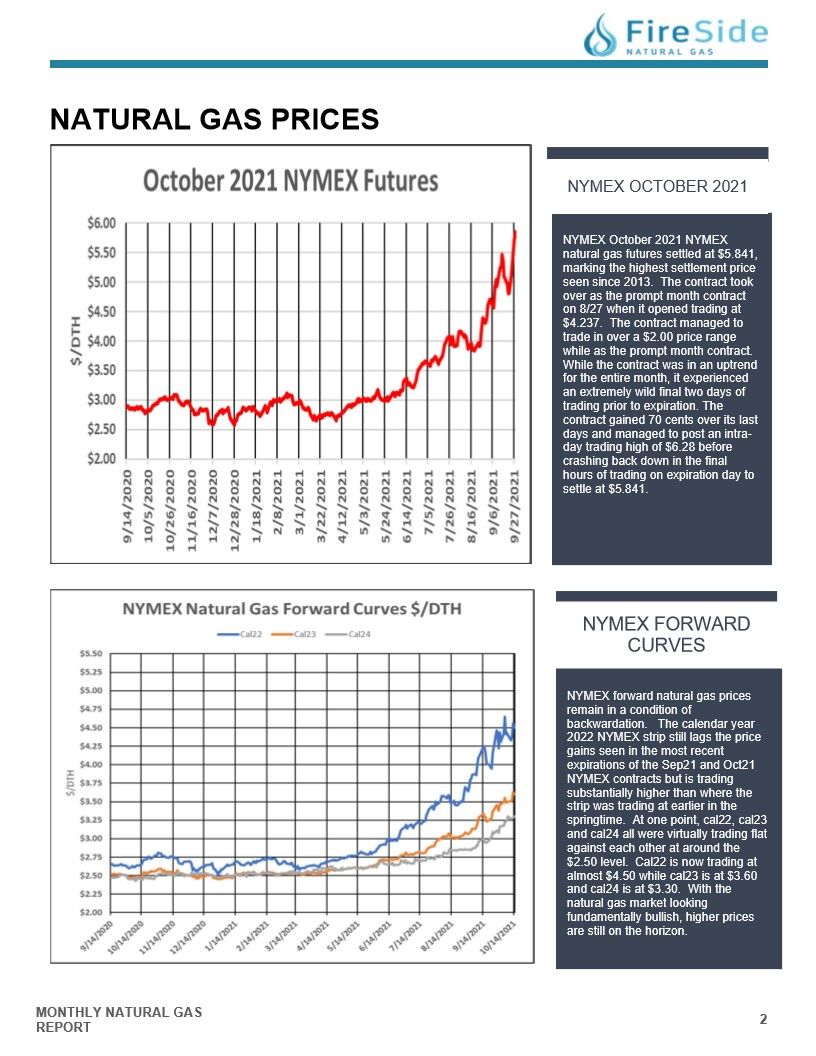

NYMEX OCTOBER 2021

NYMEX October 2021 NYMEX

natural gas futures settled at $5.841,

marking the highest settlement price

seen since 2013. The contract took

over as the prompt month contract

on 8/27 when it opened trading at

$4.237. The contract managed to

trade in over a $2.00 price range

while as the prompt month contract.

While the contract was in an uptrend

for the entire month, it experienced

an extremely wild final two days of

trading prior to expiration. The

contract gained 70 cents over its last

days and managed to post an intraday trading high of $6.28 before

crashing back down in the final

hours of trading on expiration day to

settle at $5.841.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of

backwardation. The calendar year

2022 NYMEX strip still lags the price

gains seen in the most recent

expirations of the Sep21 and Oct21

NYMEX contracts but is trading

substantially higher than where the

strip was trading at earlier in the

springtime. At one point, cal22, cal23

and cal24 all were virtually trading flat

against each other at around the

$2.50 level. Cal22 is now trading at

almost $4.50 while cal23 is at $3.60

and cal24 is at $3.30. With the

natural gas market looking

fundamentally bullish, higher prices

are still on the horizon.

NATURAL GAS SUPPLY - US DAILY PRODUCTION

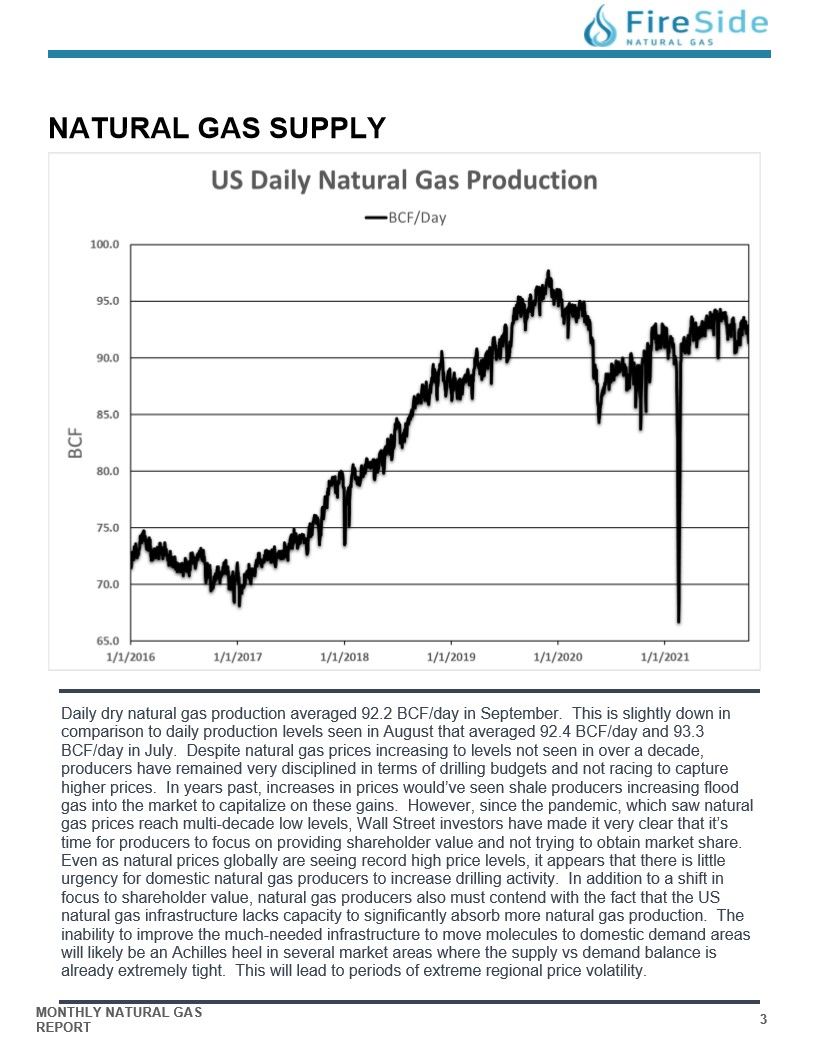

Daily dry natural gas production averaged 92.2 BCF/day in September. This is slightly down in

comparison to daily production levels seen in August that averaged 92.4 BCF/day and 93.3

BCF/day in July. Despite natural gas prices increasing to levels not seen in over a decade,

producers have remained very disciplined in terms of drilling budgets and not racing to capture

higher prices. In years past, increases in prices would've seen shale producers increasing flood

gas into the market to capitalize on these gains. However, since the pandemic, which saw natural

gas prices reach multi-decade low levels, Wall Street investors have made it very clear that it's

time for producers to focus on providing shareholder value and not trying to obtain market share.

Even as natural prices globally are seeing record high price levels, it appears that there is little

urgency for domestic natural gas producers to increase drilling activity. In addition to a shift in

focus to shareholder value, natural gas producers also must contend with the fact that the US

natural gas infrastructure lacks capacity to significantly absorb more natural gas production. The

inability to improve the much-needed infrastructure to move molecules to domestic demand areas

will likely be an Achilles heel in several market areas where the supply vs demand balance is

already extremely tight. This will lead to periods of extreme regional price volatility.

US NATURAL GAS DEMAND

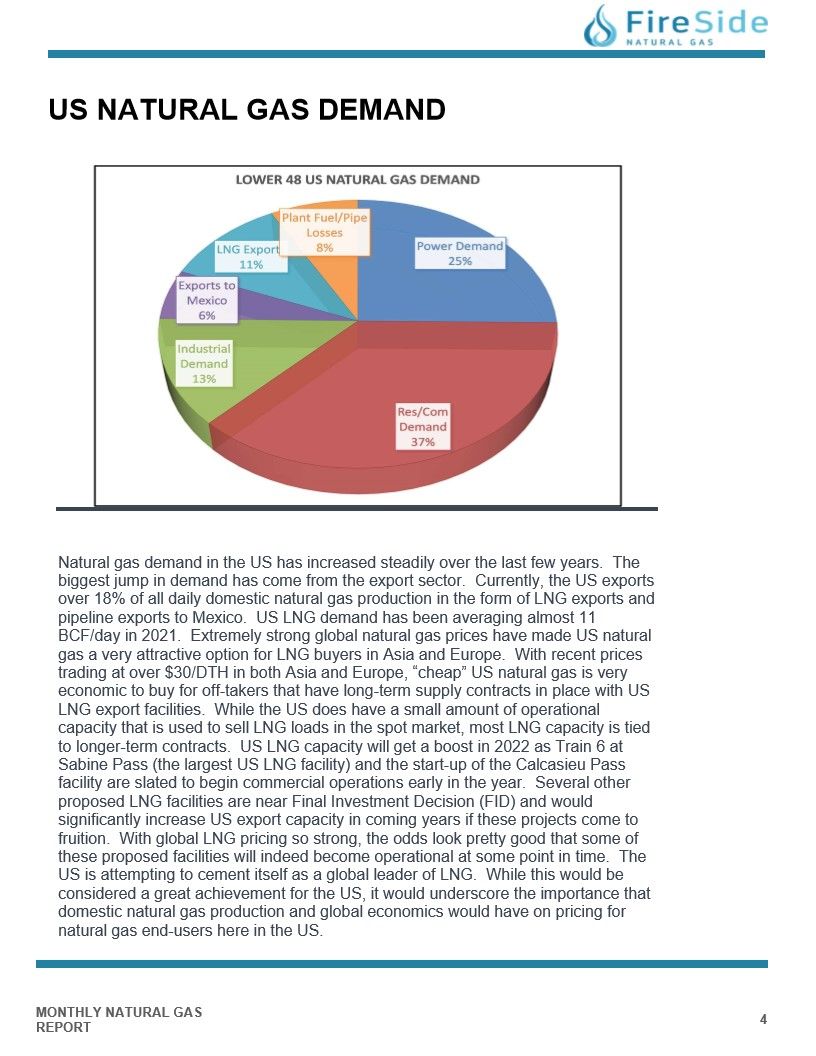

Natural gas demand in the US has increased steadily over the last few years. The

biggest jump in demand has come from the export sector. Currently, the US exports

over 18% of all daily domestic natural gas production in the form of LNG exports and

pipeline exports to Mexico. US LNG demand has been averaging almost 11

BCF/day in 2021. Extremely strong global natural gas prices have made US natural

gas a very attractive option for LNG buyers in Asia and Europe. With recent prices

trading at over $30/DTH in both Asia and Europe, "cheap" US natural gas is very

economic to buy for off-takers that have long-term supply contracts in place with US

LNG export facilities. While the US does have a small amount of operational

capacity that is used to sell LNG loads in the spot market, most LNG capacity is tied

to longer-term contracts. US LNG capacity will get a boost in 2022 as Train 6 at

Sabine Pass (the largest US LNG facility) and the start-up of the Calcasieu Pass

facility are slated to begin commercial operations early in the year. Several other

proposed LNG facilities are near Final Investment Decision (FID) and would

significantly increase US export capacity in coming years if these projects come to

fruition. With global LNG pricing so strong, the odds look pretty good that some of

these proposed facilities will indeed become operational at some point in time. The

US is attempting to cement itself as a global leader of LNG. While this would be

considered a great achievement for the US, it would underscore the importance that

domestic natural gas production and global economics would have on pricing for

natural gas end-users here in the US.

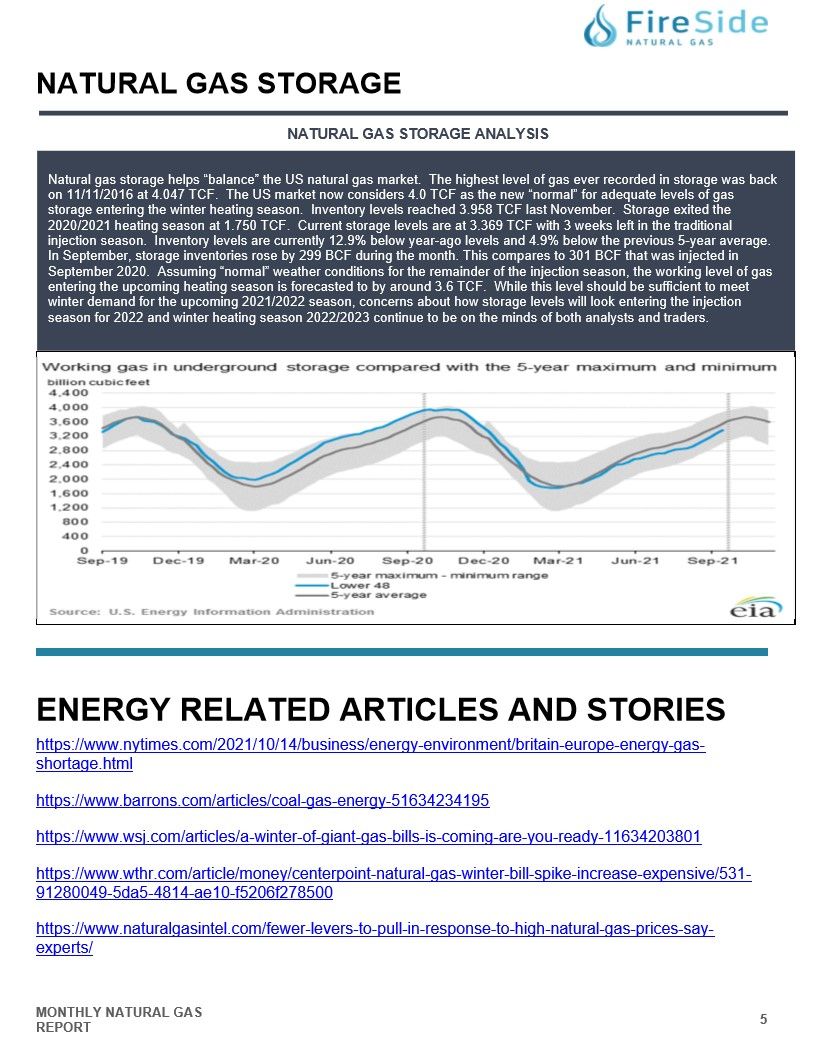

NATURAL GAS STORAGE ANALYSIS

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back

on 11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas

storage entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the

2020/2021 heating season at 1.750 TCF. Current storage levels are at 3.369 TCF with 3 weeks left in the traditional

injection season. Inventory levels are currently 12.9% below year-ago levels and 4.9% below the previous 5-year average.

In September, storage inventories rose by 299 BCF during the month. This compares to 301 BCF that was injected in

September 2020. Assuming "normal" weather conditions for the remainder of the injection season, the working level of gas

entering the upcoming heating season is forecasted to by around 3.6 TCF. While this level should be sufficient to meet

winter demand for the upcoming 2021/2022 season, concerns about how storage levels will look entering the injection

season for 2022 and winter heating season 2022/2023 continue to be on the minds of both analysts and traders.

ENERGY RELATED ARTICLES AND STORIES

https://www.barrons.com/articles/coal-gas-energy-51634234195.

https://www.wsj.com/articles/a-winter-of-giant-gas-bills-is-coming-are-you-ready-11634203801