The Weekly Natural Gas Market Newsletter October 18, 2021

The Weekly Natural Gas Market Newsletter

October 18, 2021

Natural Gas News & Notes

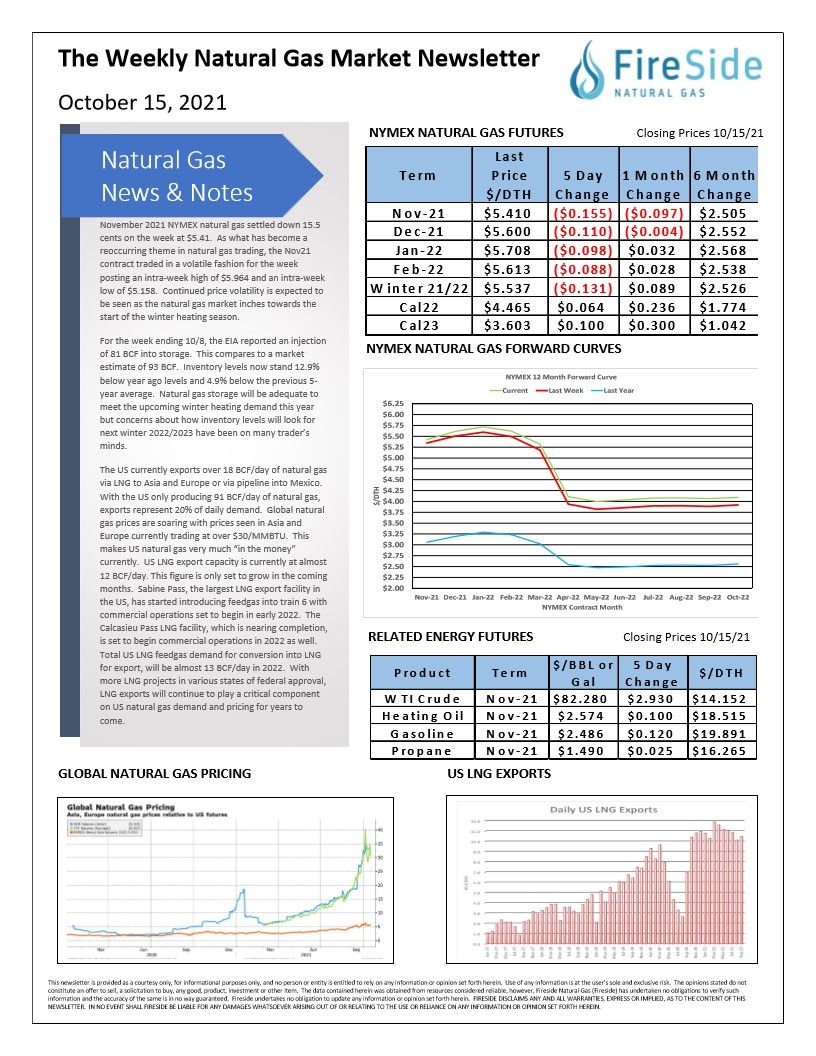

November 2021 NYMEX natural gas settled down 15.5 cents on the week at $5.41. As what has become a reoccurring theme in natural gas trading, the Nov21 contract traded in a volatile fashion for the week posting an intra-week high of $5.964 and an intra-week low of $5.158. Continued price volatility is expected to be seen as the natural gas market inches towards the start of the winter heating season.

For the week ending 10/8, the EIA reported an injection of 81 BCF into storage. This compares to a market estimate of 93 BCF. Inventory levels now stand 12.9% below year ago levels and 4.9% below the previous 5- year average. Natural gas storage will be adequate to meet the upcoming winter heating demand this year but concerns about how inventory levels will look for next winter 2022/2023 have been on many trader's minds.

The US currently exports over 18 BCF/day of natural gas

via LNG to Asia and Europe or via pipeline into Mexico.

With the US only producing 91 BCF/day of natural gas,

exports represent 20% of daily demand. Global natural

gas prices are soaring with prices seen in Asia and

Europe currently trading at over $30/MMBTU. This

makes US natural gas very much "in the money"

currently. US LNG export capacity is currently at almost

12 BCF/day. This figure is only set to grow in the coming

months. Sabine Pass, the largest LNG export facility in

the US, has started introducing feedgas into train 6 with

commercial operations set to begin in early 2022. The

Calcasieu Pass LNG facility, which is nearing completion,

is set to begin commercial operations in 2022 as well.

Total US LNG feedgas demand for conversion into LNG

for export, will be almost 13 BCF/day in 2022. With

more LNG projects in various states of federal approval,

LNG exports will continue to play a critical component

on US natural gas demand and pricing for years to

come.