The Weekly Natural Gas Market Newsletter November 27 2021

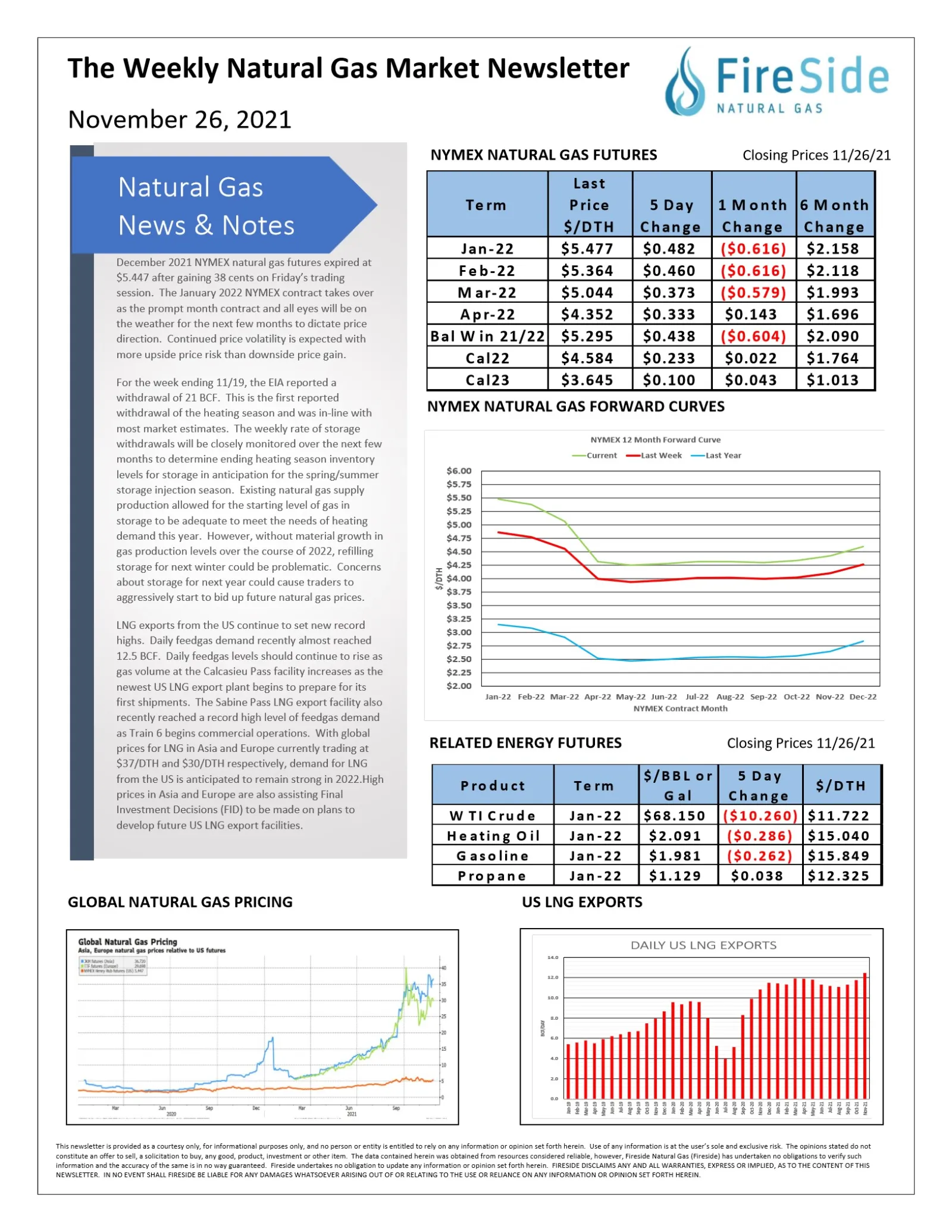

December 2021 NYMEX natural gas futures expired at $5.447 after gaining 38 cents on Friday's trading session. The January 2022 NYMEX contract takes over as the prompt month contract and all eyes will be on the weather for the next few months to dictate price direction. Continued price volatility is expected with more upside price risk than downside price gain.

For the week ending 11/19, the EIA reported a withdrawal of 21 BCF. This is the first reported withdrawal of the heating season and was in-line with most market estimates. The weekly rate of storage withdrawals will be closely monitored over the next few months to determine ending heating season inventory levels for storage in anticipation for the spring/summer storage injection season. Existing natural gas supply production allowed for the starting level of gas in storage to be adequate to meet the needs of heating demand this year. However, without material growth in gas production levels over the course of 2022, refilling storage for next winter could be problematic. Concerns about storage for next year could cause traders to aggressively start to bid up future natural gas prices.

LNG exports from the US continue to set new record highs. Daily feedgas demand recently almost reached 12.5 BCF. Daily feedgas levels should continue to rise as gas volume at the Calcasieu Pass facility increases as the newest US LNG export plan begins to prepare for its first shipments. The Sabine Pass LNG export facility also recently reached a record high level of feedgas demand as Train 6 begins commercial operations. With global prices for LNG in Asia and Europe currently trading at $37/DTH and $30/DTH respectively, demand for LNG from the US is anticipated to remain strong in 2022. High prices in Asia and Europe are also assisting Final Investment Decisions (FID) to be made on plans to develop future US LNG export facilities.