The Monthly Natural Gas Market Newsletter - November 2022

FireSide Natural Gas Monthly Report - November 2022

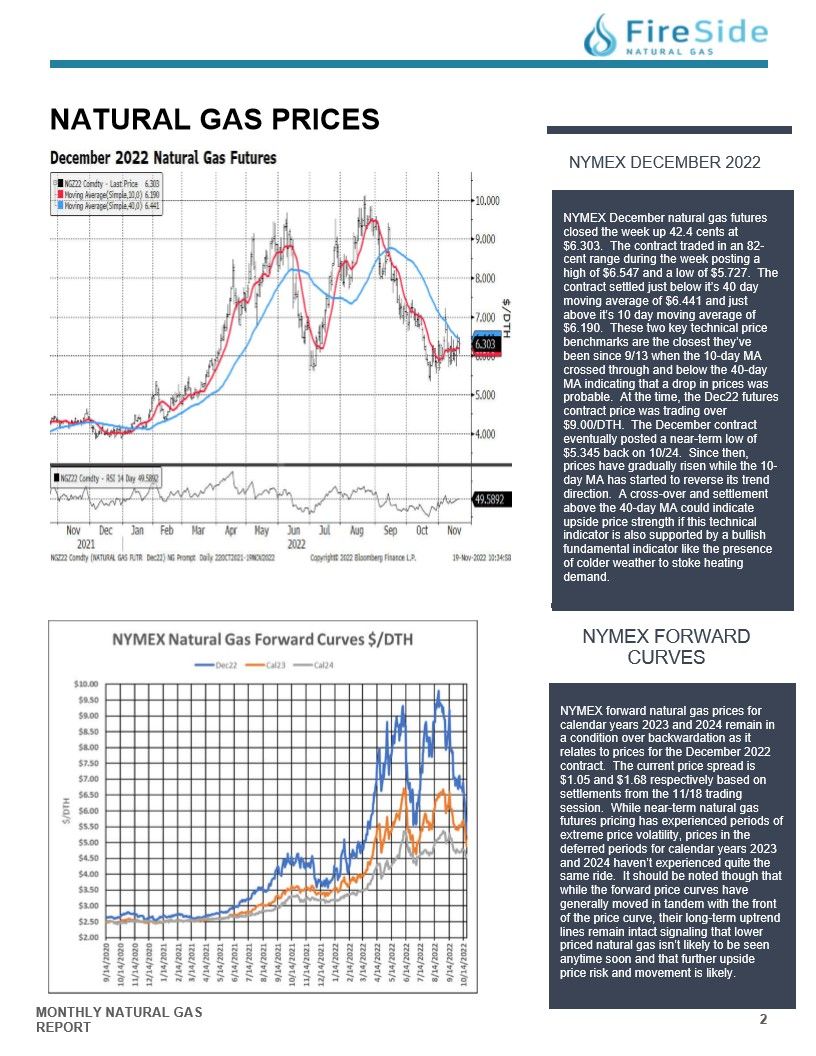

Natural Gas Prices

NYMEX DECEMBER 2022

NYMEX December natural gas futures

closed the week up 42.4 cents at

$6.303. The contract traded in an 82-

cent range during the week posting a

high of $6.547 and a low of $5.727. The

contract settled just below it's 40 day

moving average of $6.441 and just

above it's 10 day moving average of

$6.190. These two key technical price

benchmarks are the closest they've

been since 9/13 when the 10-day MA

crossed through and below the 40-day

MA indicating that a drop in prices was

probable. At the time, the Dec22 futures

contract price was trading over

$9.00/DTH. The December contract

eventually posted a near-term low of

$5.345 back on 10/24. Since then,

prices have gradually risen while the 10-

day MA has started to reverse its trend

direction. A cross-over and settlement

above the 40-day MA could indicate

upside price strength if this technical

indicator is also supported by a bullish

fundamental indicator like the presence

of colder weather to stoke heating

demand.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices for

calendar years 2023 and 2024 remain in

a condition over backwardation as it

relates to prices for the December 2022

contract. The current price spread is

$1.05 and $1.68 respectively based on

settlements from the 11/18 trading

session. While near-term natural gas

futures pricing has experienced periods of

extreme price volatility, prices in the

deferred periods for calendar years 2023

and 2024 haven't experienced quite the

same ride. It should be noted though that

while the forward price curves have

generally moved in tandem with the front

of the price curve, their long-term uptrend

lines remain intact signaling that lower

priced natural gas isn't likely to be seen

anytime soon and that further upside

price risk and movement is likely.

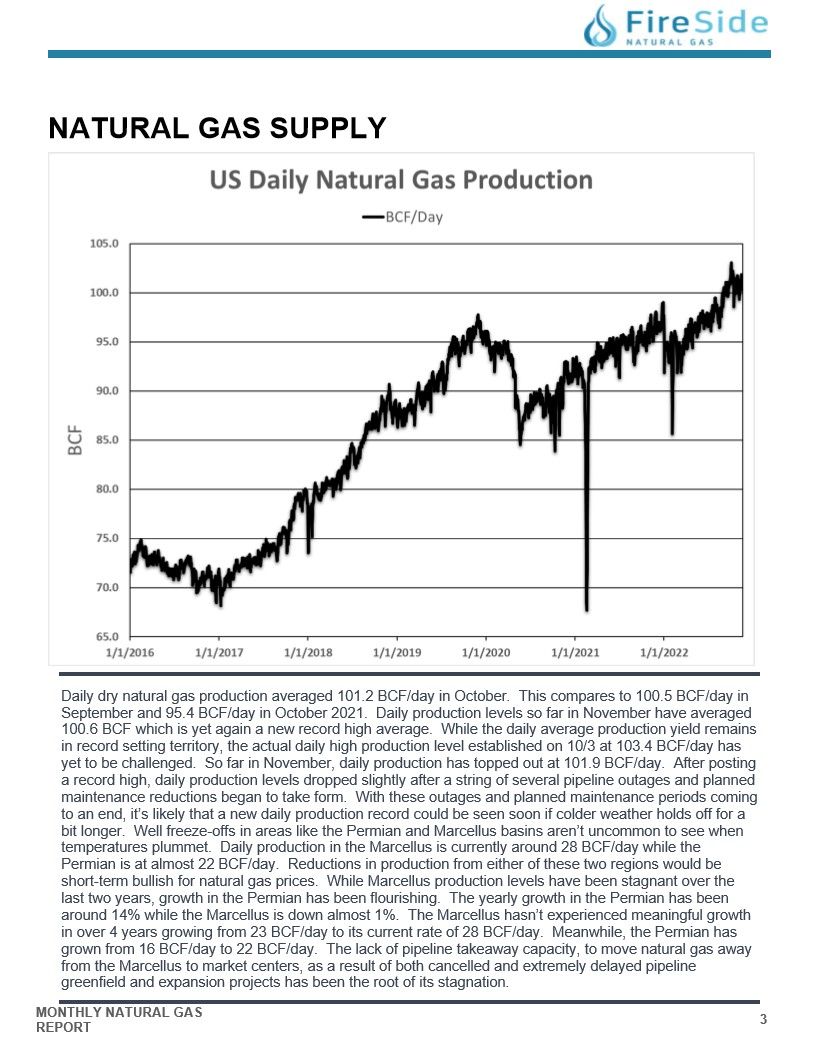

US DAILY NATURAL GAS PRODUCTION

Daily dry natural gas production averaged 101.2 BCF/day in October. This compares to 100.5 BCF/day in September and 95.4 BCF/day in October 2021. Daily production levels so far in November have averaged 100.6 BCF which is yet again a new record high average. While the daily average production yield remains in record setting territory, the actual daily high production level established on 10/3 at 103.4 BCF/day has yet to be challenged. So far in November, daily production has topped out at 101.9 BCF/day. After posting a record high, daily production levels dropped slightly after a string of several pipeline outages and planned maintenance reductions began to take form. With these outages and planned maintenance periods coming to an end, it's likely that a new daily production record could be seen soon if colder weather holds off for a bit longer. Well freeze-offs in areas like the Permian and Marcellus basins aren't uncommon to see when temperatures plummet. Daily production in the Marcellus is currently around 28 BCF/day while the Permian is at almost 22 BCF/day. Reductions in production from either of these two regions would be short-term bullish for natural gas prices. While Marcellus production levels have been stagnant over the last two years, growth in the Permian has been flourishing. The yearly growth in the Permian has been around 14% while the Marcellus is down almost 1%. The Marcellus hasn't experienced meaningful growth in over 4 years growing from 23 BCF/day to its current rate of 28 BCF/day. Meanwhile, the Permian has grown from 16 BCF/day to 22 BCF/day. The lack of pipeline takeaway capacity, to move natural gas away from the Marcellus to market centers, as a result of both cancelled and extremely delayed pipeline greenfield and expansion projects has been the root of its stagnation.

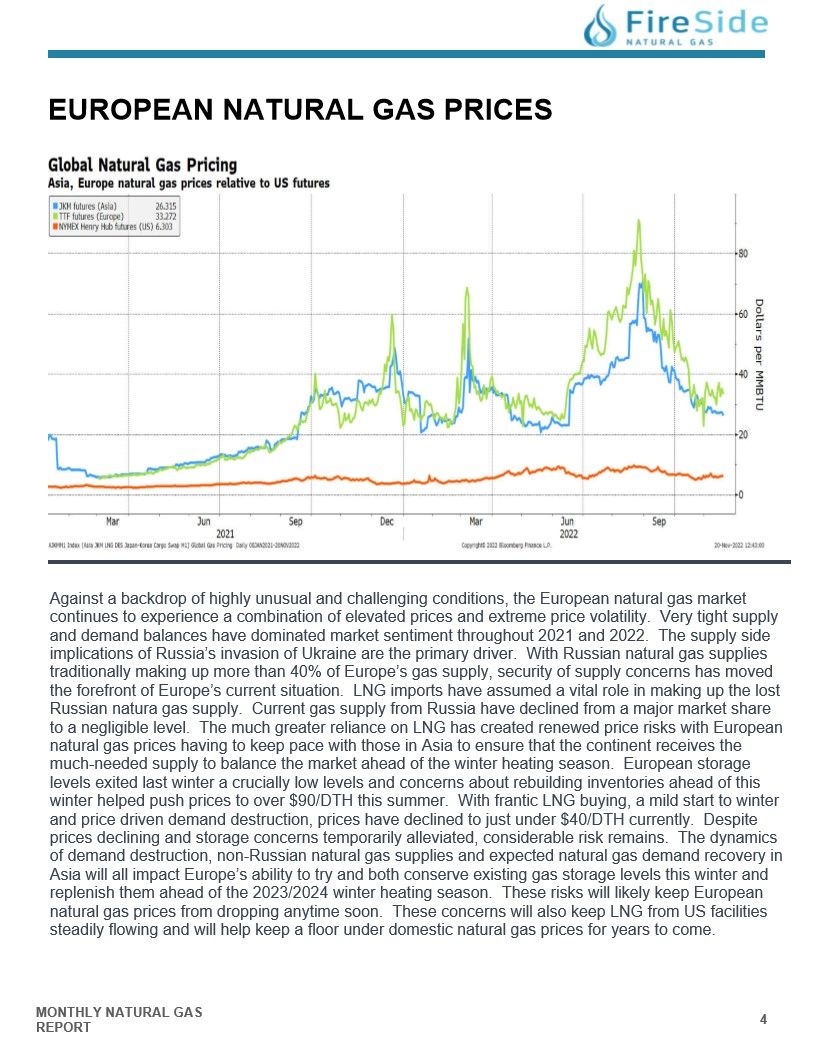

EUROPEAN NATURAL GAS PRICES

Against a backdrop of highly unusual and challenging conditions, the European natural gas market continues to experience a combination of elevated prices and extreme price volatility. Very tight supply and demand balances have dominated market sentiment throughout 2021 and 2022. The supply side implications of Russia's invasion of Ukraine are the primary driver. With Russian natural gas supplies traditionally making up more than 40% of Europe's gas supply, security of supply concerns has moved the forefront of Europe's current situation. LNG imports have assumed a vital role in making up the lost Russian natura gas supply. Current gas supply from Russia have declined from a major market share to a negligible level. The much greater reliance on LNG has created renewed price risks with European natural gas prices having to keep pace with those in Asia to ensure that the continent receives the much-needed supply to balance the market ahead of the winter heating season. European storage levels exited last winter a crucially low levels and concerns about rebuilding inventories ahead of this winter helped push prices to over $90/DTH this summer. With frantic LNG buying, a mild start to winter and price driven demand destruction, prices have declined to just under $40/DTH currently. Despite prices declining and storage concerns temporarily alleviated, considerable risk remains. The dynamics of demand destruction, non-Russian natural gas supplies and expected natural gas demand recovery in Asia will all impact Europe's ability to try and both conserve existing gas storage levels this winter and replenish them ahead of the 2023/2024 winter heating season. These risks will likely keep European natural gas prices from dropping anytime soon. These concerns will also keep LNG from US facilities steadily flowing and will help keep a floor under domestic natural gas prices for years to come.

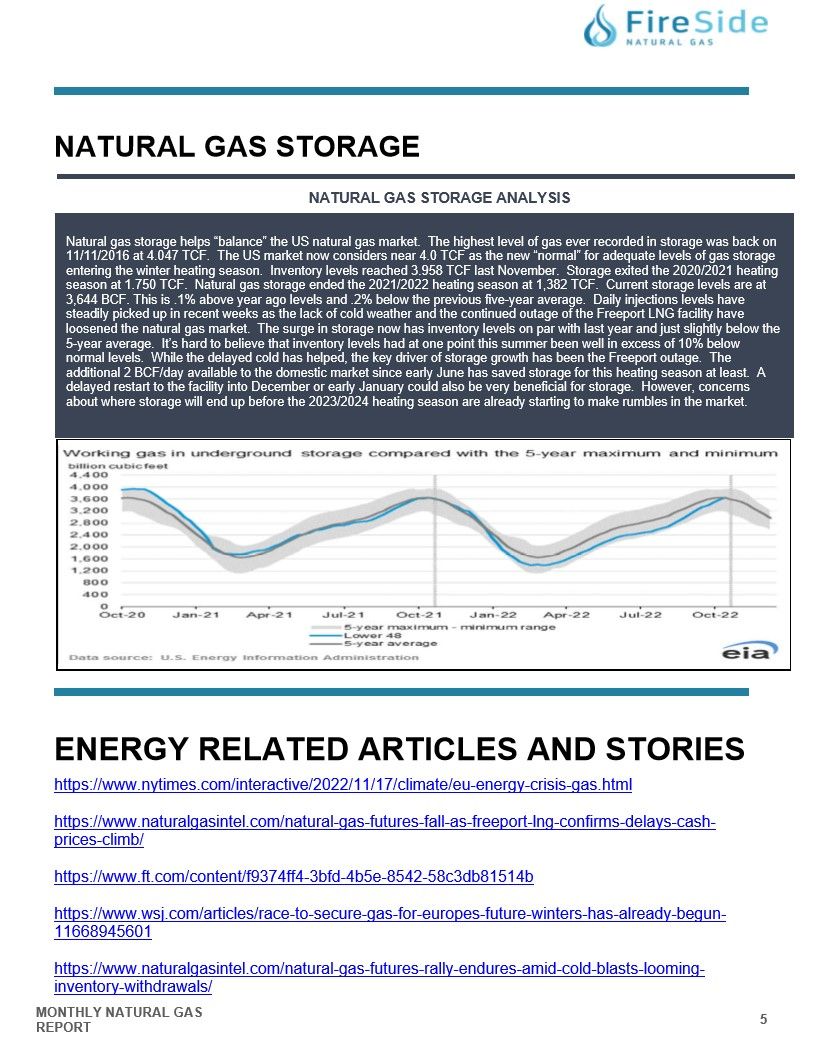

NATURAL GAS STORAGE ANALYSIS

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on

11/11/2016 at 4.047 TCF. The US market now considers near 4.0 TCF as the new "normal" for adequate levels of gas storage

entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating

season at 1.750 TCF. Natural gas storage ended the 2021/2022 heating season at 1,382 TCF. Current storage levels are at

3,644 BCF. This is .1% above year ago levels and .2% below the previous five-year average. Daily injections levels have

steadily picked up in recent weeks as the lack of cold weather and the continued outage of the Freeport LNG facility have

loosened the natural gas market. The surge in storage now has inventory levels on par with last year and just slightly below the

5-year average. It's hard to believe that inventory levels had at one point this summer been well in excess of 10% below

normal levels. While the delayed cold has helped, the key driver of storage growth has been the Freeport outage. The

additional 2 BCF/day available to the domestic market since early June has saved storage for this heating season at least. A

delayed restart to the facility into December or early January could also be very beneficial for storage. However, concerns

about where storage will end up before the 2023/2024 heating season are already starting to make rumbles in the market.

ENERGY RELATED ARTICLES AND STORIES

Europe's Energy Risks Go Beyond Natural Gas - The New York Times (nytimes.com)

Subscribe to read | Financial Times (ft.com)

Race to Secure Gas for Europe's Future Winters Has Already Begun - WSJ