The Monthly Natural Gas Market Newsletter - November 2021

FireSide Natural Gas

Monthly Report

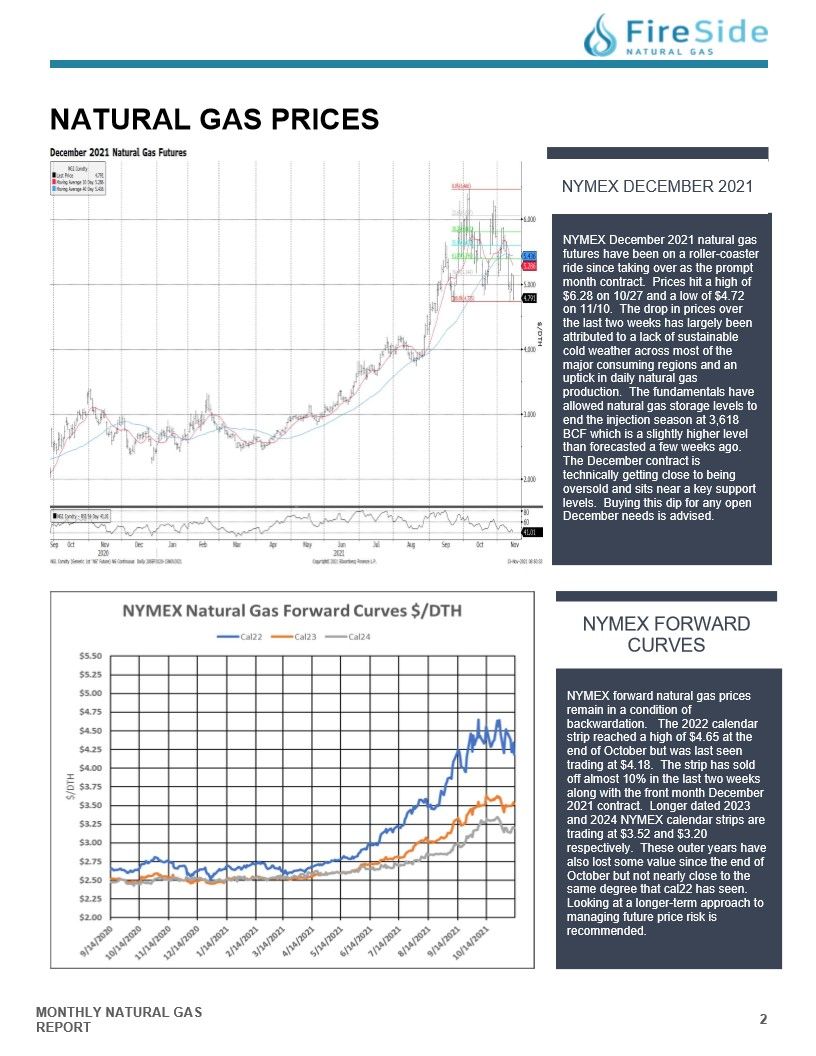

Natural Gas Prices

NYMEX DECEMBER 2021

NYMEX December 2021 natural gas

futures have been on a roller-coaster

ride since taking over as the prompt

month contract. Prices hit a high of

$6.28 on 10/27 and a low of $4.72

on 11/10. The drop in prices over

the last two weeks has largely been

attributed to a lack of sustainable

cold weather across most of the

major consuming regions and an

uptick in daily natural gas

production. The fundamentals have

allowed natural gas storage levels to

end the injection season at 3,618

BCF which is a slightly higher level

than forecasted a few weeks ago.

The December contract is

technically getting close to being

oversold and sits near a key support

levels. Buying this dip for any open

December needs is advised.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of

backwardation. The 2022 calendar

strip reached a high of $4.65 at the

end of October but was last seen

trading at $4.18. The strip has sold

off almost 10% in the last two weeks

along with the front month December

2021 contract. Longer dated 2023

and 2024 NYMEX calendar strips are

trading at $3.52 and $3.20

respectively. These outer years have

also lost some value since the end of

October but not nearly close to the

same degree that cal22 has seen.

Looking at a longer-term approach to

managing future price risk is

recommended.

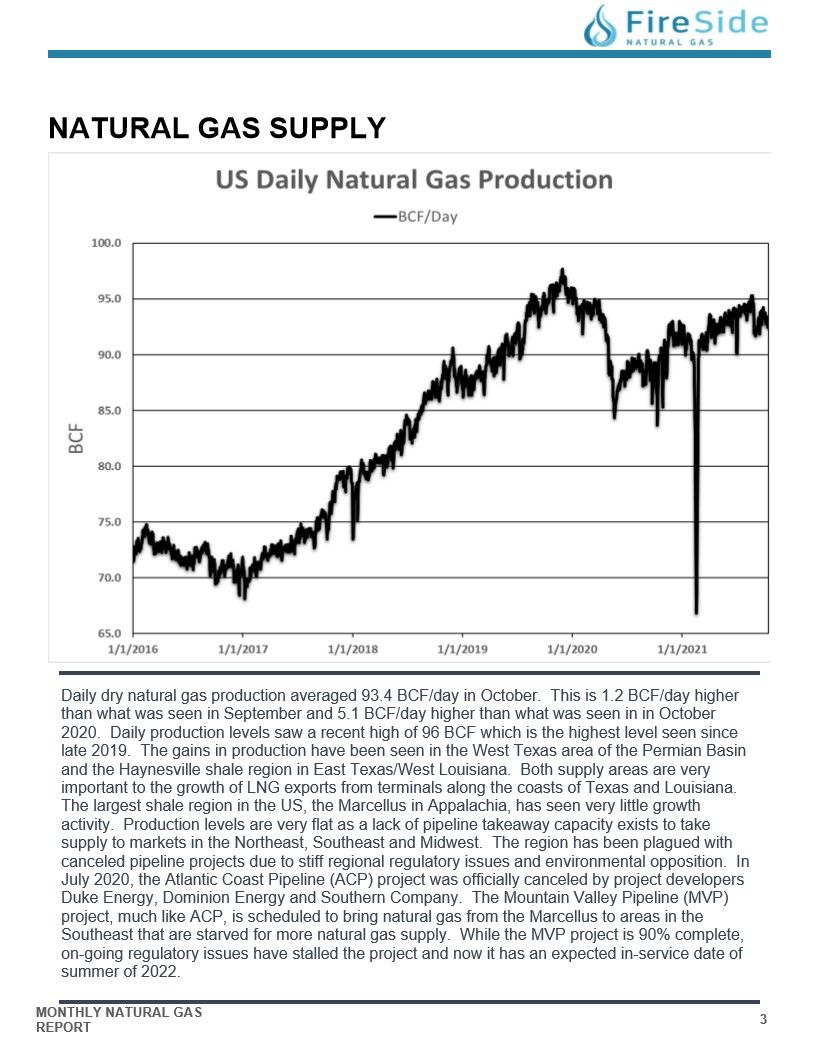

NATURAL GAS SUPPLY - US PRODUCTION

Daily dry natural gas production averaged 93.4 BCF/day in October. This is 1.2 BCF/day higher

than what was seen in September and 5.1 BCF/day higher than what was seen in in October

2020. Daily production levels saw a recent high of 96 BCF which is the highest level seen since

late 2019. The gains in production have been seen in the West Texas area of the Permian Basin

and the Haynesville shale region in East Texas/West Louisiana. Both supply areas are very

important to the growth of LNG exports from terminals along the coasts of Texas and Louisiana.

The largest shale region in the US, the Marcellus in Appalachia, has seen very little growth

activity. Production levels are very flat as a lack of pipeline takeaway capacity exists to take

supply to markets in the Northeast, Southeast and Midwest. The region has been plagued with

canceled pipeline projects due to stiff regional regulatory issues and environmental opposition. In

July 2020, the Atlantic Coast Pipeline (ACP) project was officially canceled by project developers

Duke Energy, Dominion Energy and Southern Company. The Mountain Valley Pipeline (MVP)

project, much like ACP, is scheduled to bring natural gas from the Marcellus to areas in the

Southeast that are starved for more natural gas supply. While the MVP project is 90% complete,

on-going regulatory issues have stalled the project and now it has an expected in-service date of

summer of 2022.

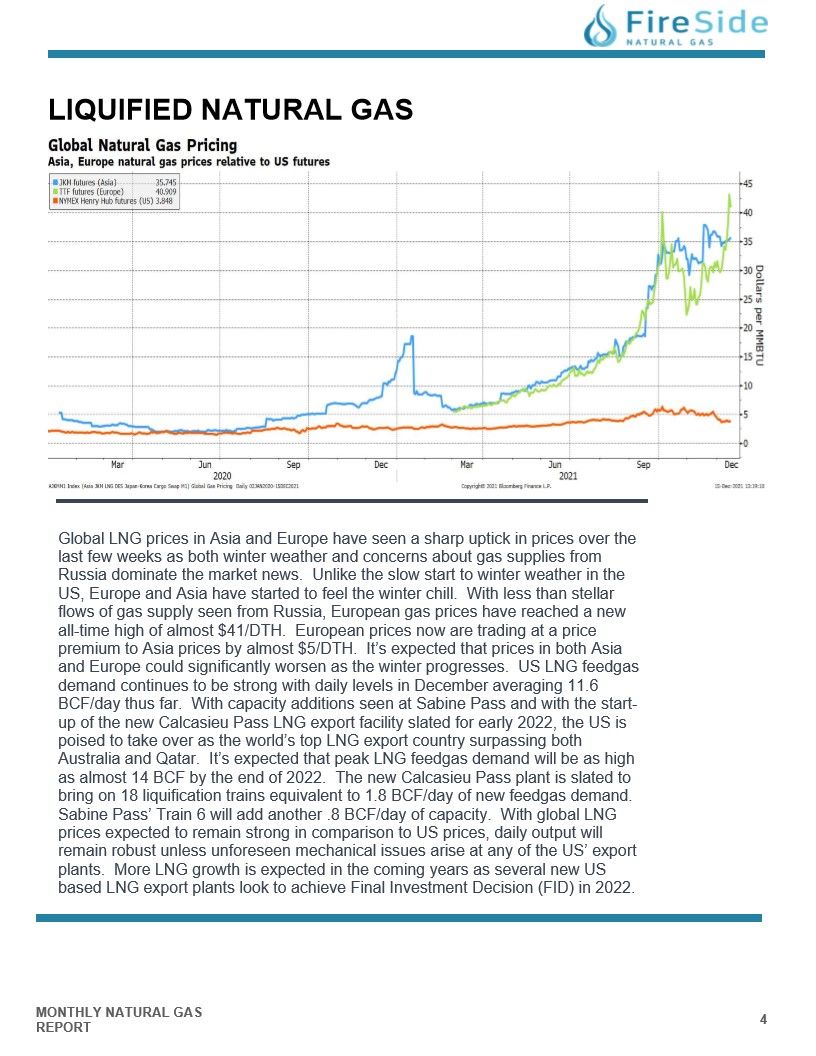

LIQUIFIED NATURAL GAS - GLOBAL PRICING

Global LNG prices in Asia and Europe remain elevated against domestic natural gas

pricing in the US. Prices in Europe have improved over the last few weeks as

Russia as agreed to export more natural gas to European countries, but prices

remain historically high heading into the peak winter heating season. Natural gas

storage levels in Europe were depleted after an extremely cold winter last year.

European storage levels remain dangerously low and depending on weather, pricing

could return to the $40/DTH level. LNG prices in Asia have lost gains over the last

few weeks as well. They remain more expensive than what's seen in Europe, at an

equivalent $31/DTH, and demand for LNG in Asia is expected to remain robust this

winter as well. LNG exports from the US should stay strong considering the price

spreads currently seen. LNG feedgas demand recently set a record high of 11.5

BCF/day. The Calcasieu Pass facility will be the newest US export terminal to

become operational in 2022. The facility has recently received FERC approval to

start accepting feedgas to produce LNG. Daily natural gas nominations to the plant

have been slowly increasing and should start to ramp-up further soon in the coming

weeks. Sabine Pass' Train 6 is also slated to become operational soon. With both

the increase in export capacity from Sabine Pass and Calcasieu Pass, record LNG

exports for the US will be seen in 2022.

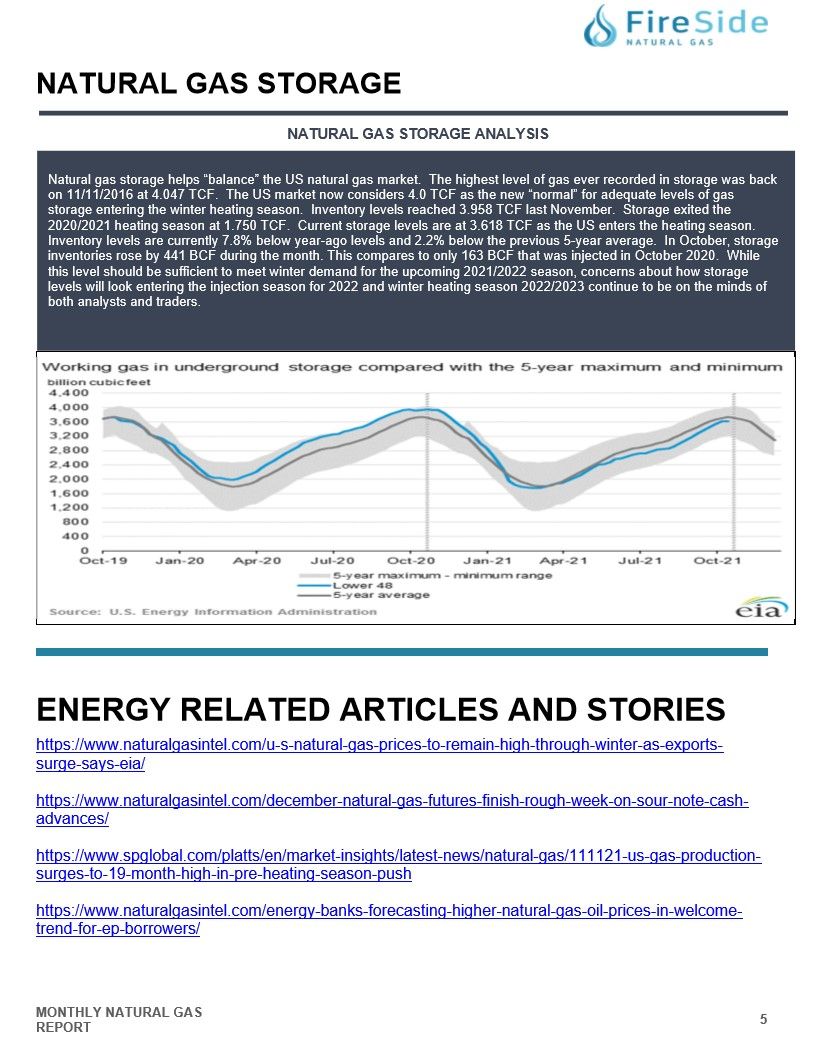

NATURAL GAS STORAGE ANALYSIS

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back

on 11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas

storage entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the

2020/2021 heating season at 1.750 TCF. Current storage levels are at 3.618 TCF as the US enters the heating season.

Inventory levels are currently 7.8% below year-ago levels and 2.2% below the previous 5-year average. In October, storage

inventories rose by 441 BCF during the month. This compares to only 163 BCF that was injected in October 2020. While

this level should be sufficient to meet winter demand for the upcoming 2021/2022 season, concerns about how storage

levels will look entering the injection season for 2022 and winter heating season 2022/2023 continue to be on the minds of

both analysts and traders.

ENERGY RELATED ARTICLES AND STORIES