The Monthly Natural Gas Market Newsletter - March 2022

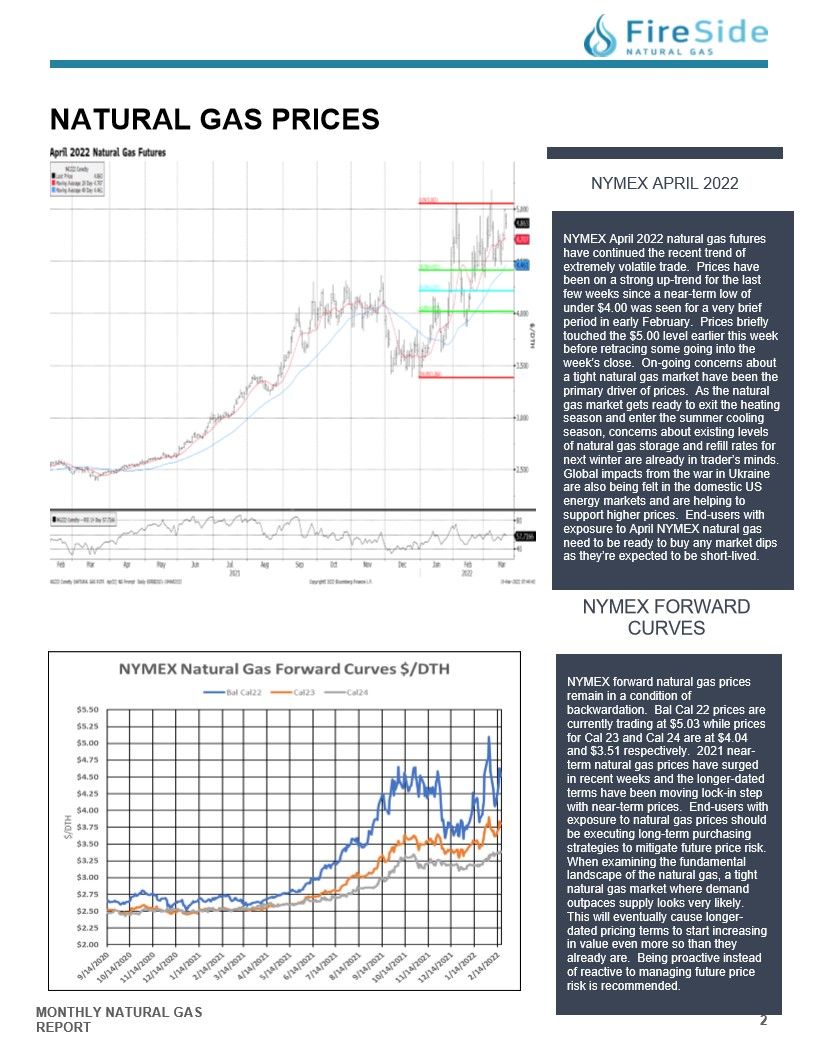

NYMEX APRIL 2022

NYMEX April 2022 natural gas futures

have continued the recent trend of

extremely volatile trade. Prices have

been on a strong up-trend for the last

few weeks since a near-term low of

under $4.00 was seen for a very brief

period in early February. Prices briefly

touched the $5.00 level earlier this week

before retracing some going into the

week's close. On-going concerns about

a tight natural gas market have been the

primary driver of prices. As the natural

gas market gets ready to exit the heating

season and enter the summer cooling

season, concerns about existing levels

of natural gas storage and refill rates for

next winter are already in trader's minds.

Global impacts from the war in Ukraine

are also being felt in the domestic US

energy markets and are helping to

support higher prices. End-users with

exposure to April NYMEX natural gas

need to be ready to buy any market dips

as they're expected to be short-lived.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of

backwardation. Bal Cal 22 prices are

currently trading at $5.03 while prices

for Cal 23 and Cal 24 are at $4.04

and $3.51 respectively. 2021 near-term natural gas prices have surged

in recent weeks and the longer-dated

terms have been moving lock-in step

with near-term prices. End-users with

exposure to natural gas prices should

be executing long-term purchasing

strategies to mitigate future price risk.

When examining the fundamental

landscape of the natural gas, a tight

natural gas market where demand

outpaces supply looks very likely.

This will eventually cause longer dated pricing terms to start increasing

in value even more so than they

already are. Being proactive instead

of reactive to managing future price

risk is recommended.

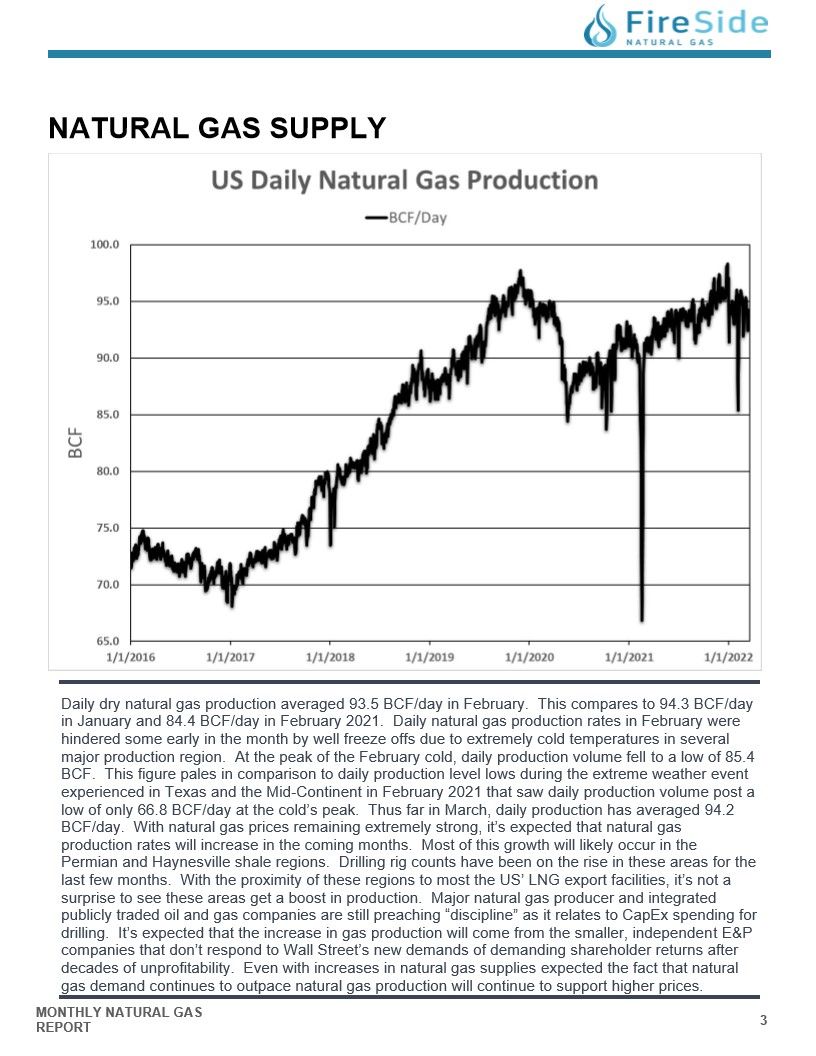

Natural Gas Supply - US Daily Natural Gas Production

Daily dry natural gas production averaged 93.5 BCF/day in February. This compares to 94.3 BCF/day

in January and 84.4 BCF/day in February 2021. Daily natural gas production rates in February were

hindered some early in the month by well freeze offs due to extremely cold temperatures in several

major production region. At the peak of the February cold, daily production volume fell to a low of 85.4

BCF. This figure pales in comparison to daily production level lows during the extreme weather event

experienced in Texas and the Mid-Continent in February 2021 that saw daily production volume post a

low of only 66.8 BCF/day at the cold's peak. Thus far in March, daily production has averaged 94.2

BCF/day. With natural gas prices remaining extremely strong, it's expected that natural gas

production rates will increase in the coming months. Most of this growth will likely occur in the

Permian and Haynesville shale regions. Drilling rig counts have been on the rise in these areas for the

last few months. With the proximity of these regions to most the US' LNG export facilities, it's not a

surprise to see these areas get a boost in production. Major natural gas producer and integrated

publicly traded oil and gas companies are still preaching "discipline" as it relates to CapEx spending for

drilling. It's expected that the increase in gas production will come from the smaller, independent E&P

companies that don't respond to Wall Street's new demands of demanding shareholder returns after

decades of unprofitability. Even with increases in natural gas supplies expected the fact that natural

gas demand continues to outpace natural gas production will continue to support higher prices.

RUSSIA/UKRAINE - IMPACTS ON US ENERGY

Global oil prices have been in turmoil since the invasion of Ukraine by Russia. NYMEX WTI crude oil futures

jumped to a high of $130/bbl at the start of the invasion. Retail gasoline prices across the country have jumped

dramatically in a similar fashion. While oil and gasoline prices get the national headlines, it's important to

remember that energy markets in general are integrated in some fashion. It would appear to the casual eye that

domestic energy markets (except for oil) in the US shouldn't be impacted by what transpires a thousand miles

away. And while that may be true directly, the situation in Ukraine certainly has a very indirect impact on the US

natural gas, electricity and coal markets. Russia provides almost 40% of natural gas supplies to Eastern Europe.

European natural gas prices have exploded since the start of the war as the fear that Russia could use their natural

gas as a "political" weapon. The US is now the world's largest exporter of Liquified Natural Gas (LNG). With

European countries desperately trying to figure out how to wean themselves off Russian natural gas, US LNG is

helping to make this happen. Exports to Europe have surged to over 70% of all US LNG cargo destinations over

the last few weeks. While the US is currently at a maximum capacity for LNG production, the situation in Ukraine

supports continued growth in LNG development in the US. This, in short, means that there will ultimately be more

natural gas supplies that aren't consumed domestically. This is a far cry from the fundamental landscape of 5

years ago when almost all natural gas produced in the US stayed in the US. In addition to Russia being the largest

supplier of natural gas to Eastern Europe, Russia is also the largest exporter of coal to the region. With natural

gas prices in Europe already extremely high, many countries are switching to coal power generation because it's a

more economic fuel source. This means that demand for coal is poised to surge, and US coal producers will be

stepping in to help meet this demand. Pricing for this expectation is already being seen as domestic coal prices

have outpaced natural gas in terms of price increases over the last few weeks. Coal has fallen out of favor in the

US over the years due to emission concerns. However, in 2021, as US natural gas prices soared, use of coal for

power generation saw its first annual increase in many years since it now became the "marginal" fuel or most cost-effective fuel source for power generation. With the continuation of US natural gas prices increasing, it was again

expected in 2022 that coal would be the marginal fuel source as the US enters the peak electricity demand season.

However, that narrative has changed completely and despite extremely high natural gas prices, coal no longer

looks like the optimal fuel to use. This means that more natural gas is expected to be used in 2022 for power

generation demand than previously estimated. This further implies that an already "tight" natural gas market will be

even tighter, and the likely result is that prices for both natural gas and electricity will continue to increase in the US

for the foreseeable future.

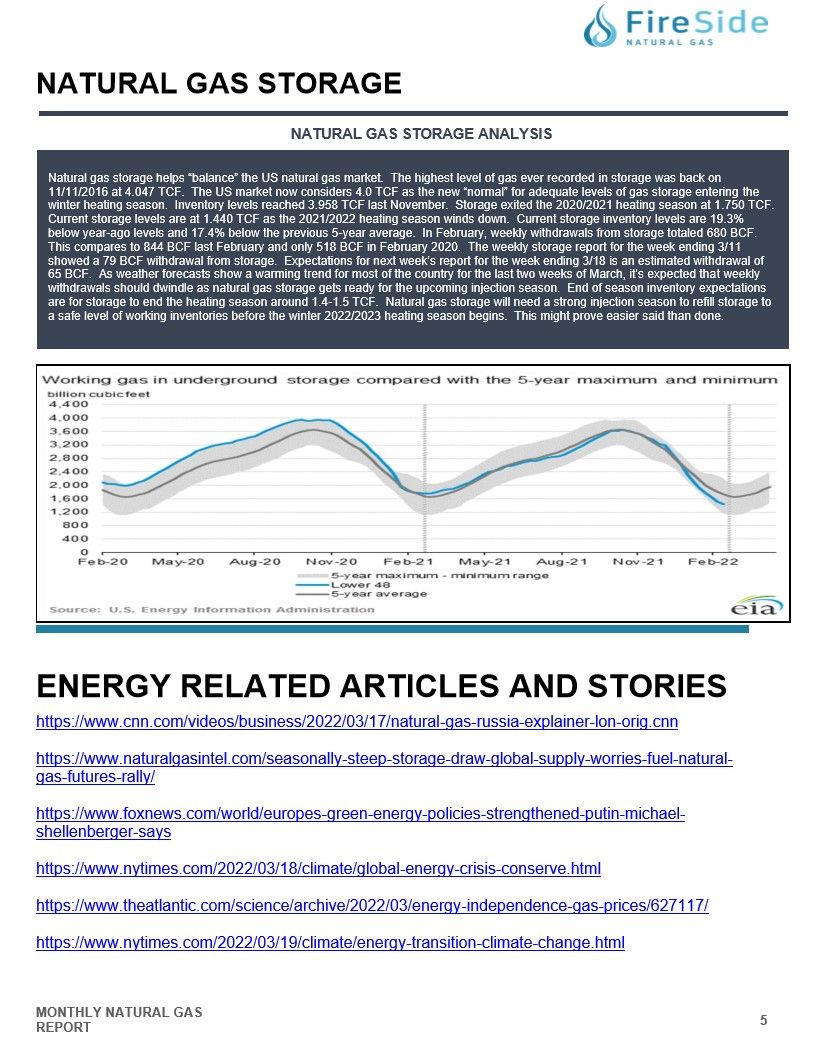

Natural Gas Storage Analysis

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on

11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas storage entering the

winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating season at 1.750 TCF.

Current storage levels are at 1.440 TCF as the 2021/2022 heating season winds down. Current storage inventory levels are 19.3%

below year-ago levels and 17.4% below the previous 5-year average. In February, weekly withdrawals from storage totaled 680 BCF.

This compares to 844 BCF last February and only 518 BCF in February 2020. The weekly storage report for the week ending 3/11

showed a 79 BCF withdrawal from storage. Expectations for next week's report for the week ending 3/18 is an estimated withdrawal of

65 BCF. As weather forecasts show a warming trend for most of the country for the last two weeks of March, it's expected that weekly

withdrawals should dwindle as natural gas storage gets ready for the upcoming injection season. End of season inventory expectations

are for storage to end the heating season around 1.4-1.5 TCF. Natural gas storage will need a strong injection season to refill storage to

a safe level of working inventories before the winter 2022/2023 heating season begins. This might prove easier said than done.

Energy Related Articles and Stories

https://www.cnn.com/videos/business/2022/03/17/natural-gas-russia-explainer-lon-orig.cnn

https://www.nytimes.com/2022/03/18/climate/global-energy-crisis-conserve.html

https://www.theatlantic.com/science/archive/2022/03/energy-independence-gas-prices/627117/

https://www.nytimes.com/2022/03/19/climate/energy-transition-climate-change.htm