The Monthly Natural Gas Market Newsletter - July 2022

FireSide Natural Gas Monthly Report - July 2022

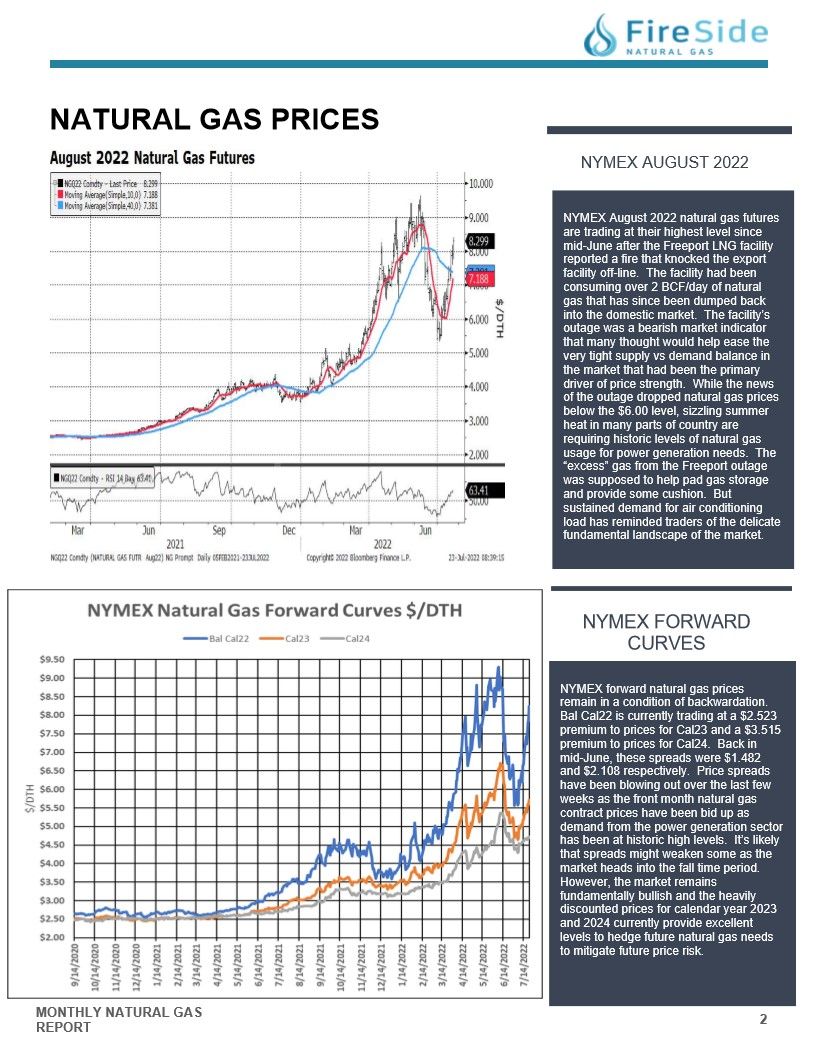

Natural Gas Prices

NYMEX AUGUST 2022

NYMEX August 2022 natural gas futures

are trading at their highest level since

mid-June after the Freeport LNG facility

reported a fire that knocked the export

facility off-line. The facility had been

consuming over 2 BCF/day of natural

gas that has since been dumped back

into the domestic market. The facility's

outage was a bearish market indicator

that many thought would help ease the

very tight supply vs demand balance in

the market that had been the primary

driver of price strength. While the news

of the outage dropped natural gas prices

below the $6.00 level, sizzling summer

heat in many parts of country are

requiring historic levels of natural gas

usage for power generation needs. The

"excess" gas from the Freeport outage

was supposed to help pad gas storage

and provide some cushion. But

sustained demand for air conditioning

load has reminded traders of the delicate

fundamental landscape of the market.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices remain in a condition of backwardation. Bal Cal22 is currently trading at a $2.523 premium to prices for Cal23 and a $3.515 premium to prices for Cal24. Back in mid-June, these spreads were $1.482 and $2.108 respectively. Price spreads have been blowing out over the last few weeks as the front month natural gas contract prices have been bid up as demand from the power generation sector has been at historic high levels. It's likely that spreads might weaken some as the market heads into the fall time period. However, the market remains fundamentally bullish and the heavily discounted prices for calendar year 2023 and 2024 currently provide excellent levels to hedge future natural gas needs to mitigate future price risk.

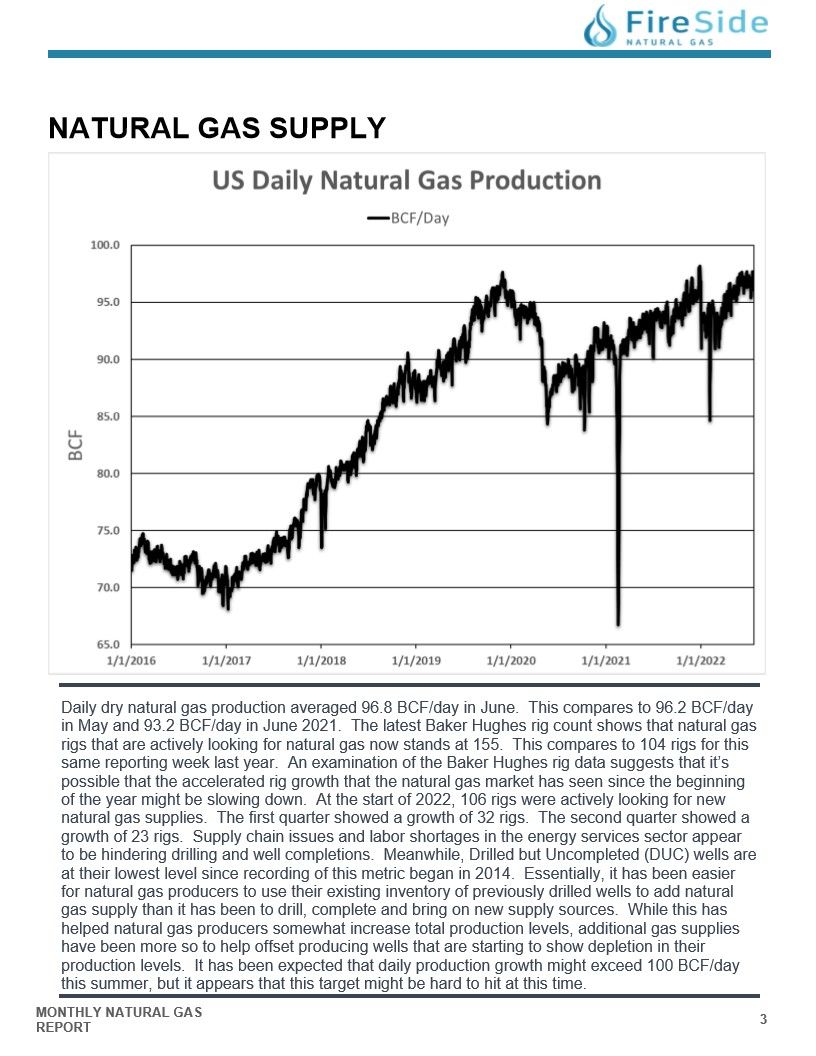

NATURAL GAS SUPPLY - US DAILY PRODUCTION

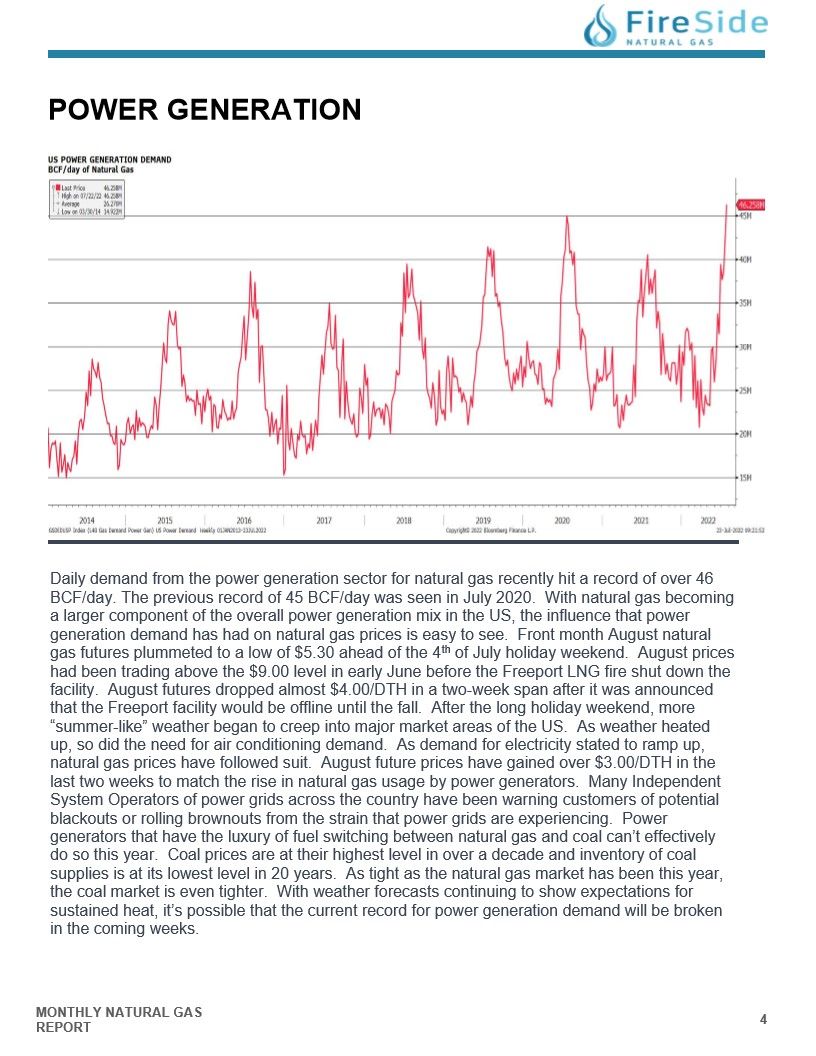

POWER GENERATION

Daily demand from the power generation sector for natural gas recently hit a record of over 46

BCF/day. The previous record of 45 BCF/day was seen in July 2020. With natural gas becoming

a larger component of the overall power generation mix in the US, the influence that power

generation demand has had on natural gas prices is easy to see. Front month August natural

gas futures plummeted to a low of $5.30 ahead of the 4th of July holiday weekend. August prices

had been trading above the $9.00 level in early June before the Freeport LNG fire shut down the

facility. August futures dropped almost $4.00/DTH in a two-week span after it was announced

that the Freeport facility would be offline until the fall. After the long holiday weekend, more

"summer-like" weather began to creep into major market areas of the US. As weather heated

up, so did the need for air conditioning demand. As demand for electricity stated to ramp up,

natural gas prices have followed suit. August future prices have gained over $3.00/DTH in the

last two weeks to match the rise in natural gas usage by power generators. Many Independent

System Operators of power grids across the country have been warning customers of potential

blackouts or rolling brownouts from the strain that power grids are experiencing. Power

generators that have the luxury of fuel switching between natural gas and coal can't effectively

do so this year. Coal prices are at their highest level in over a decade and inventory of coal

supplies is at its lowest level in 20 years. As tight as the natural gas market has been this year,

the coal market is even tighter. With weather forecasts continuing to show expectations for

sustained heat, it's possible that the current record for power generation demand will be broken

in the coming weeks.

NATURAL GAS STORAGE ANALYSIS

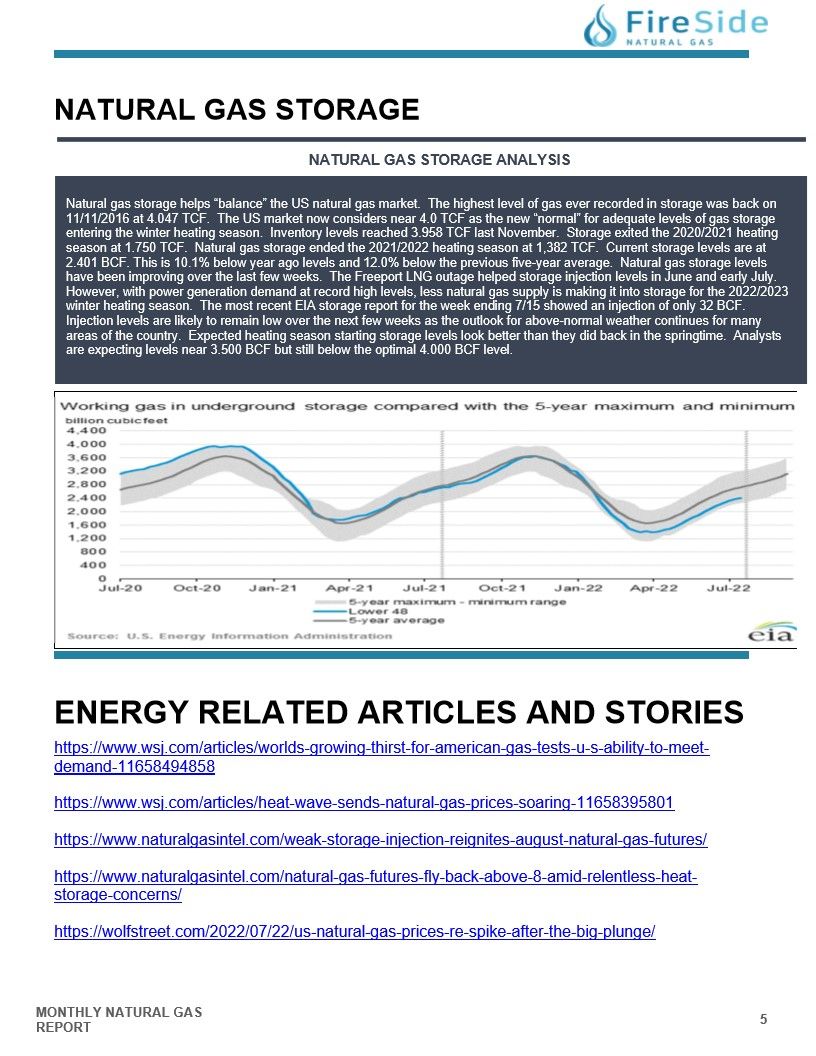

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on

11/11/2016 at 4.047 TCF. The US market now considers near 4.0 TCF as the new "normal" for adequate levels of gas storage

entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating

season at 1.750 TCF. Natural gas storage ended the 2021/2022 heating season at 1,382 TCF. Current storage levels are at

2.401 BCF. This is 10.1% below year ago levels and 12.0% below the previous five-year average. Natural gas storage levels

have been improving over the last few weeks. The Freeport LNG outage helped storage injection levels in June and early July.

However, with power generation demand at record high levels, less natural gas supply is making it into storage for the 2022/2023

winter heating season. The most recent EIA storage report for the week ending 7/15 showed an injection of only 32 BCF.

Injection levels are likely to remain low over the next few weeks as the outlook for above-normal weather continues for many

areas of the country. Expected heating season starting storage levels look better than they did back in the springtime. Analysts

are expecting levels near 3.500 BCF but still below the optimal 4.000 BCF level.

World's Growing Thirst for American Gas Tests U.S. Ability to Meet Demand - WSJ

Heat Wave Sends Natural-Gas Prices Soaring - WSJ

Weak Storage Injection Reignites August Natural Gas Futures - Natural Gas Intelligence

US Natural Gas Prices Re-Spike, after the Big Plunge | Wolf Street