The Monthly Natural Gas Market Newsletter - January Report

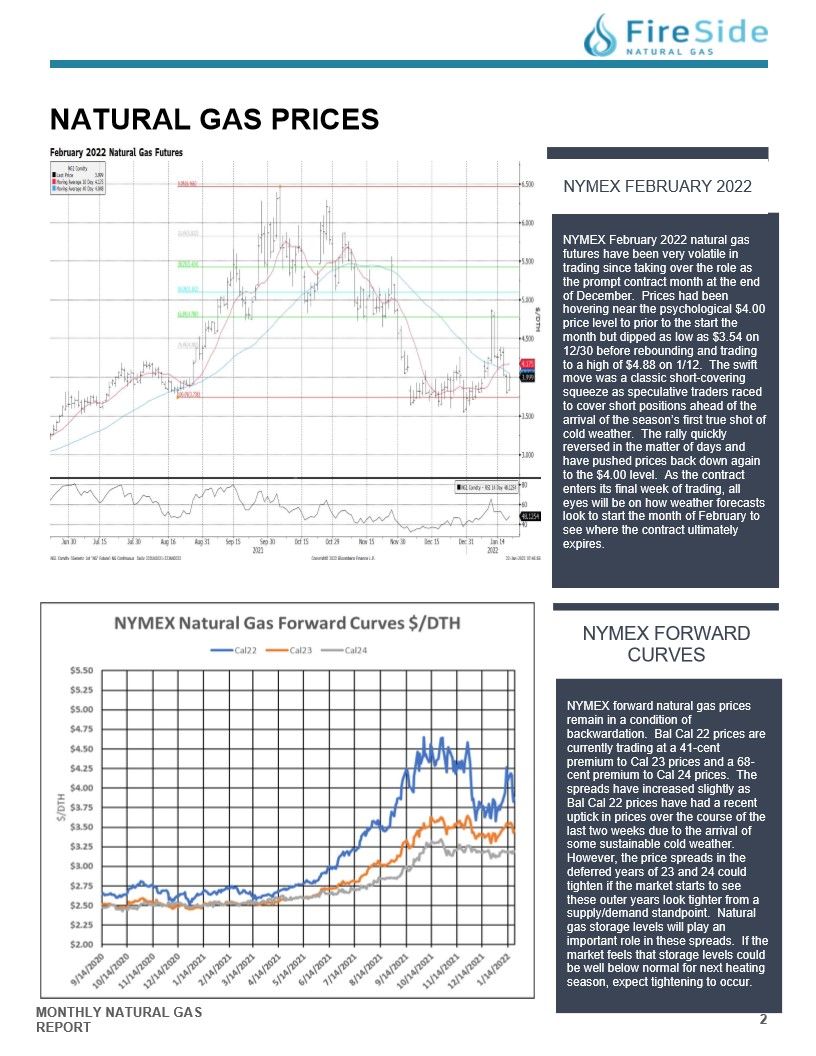

NATURAL GAS PRICES - NYMEX FEBRUARY 2022

NYMEX February 2022 natural gas

futures have been very volatile in

trading since taking over the role as

the prompt contract month at the end

of December. Prices had been

hovering near the psychological $4.00

price level to prior to the start the

month but dipped as low as $3.54 on

12/30 before rebounding and trading

to a high of $4.88 on 1/12. The swift

move was a classic short-covering

squeeze as speculative traders raced

to cover short positions ahead of the

arrival of the season's first true shot of

cold weather. The rally quickly

reversed in the matter of days and

have pushed prices back down again

to the $4.00 level. As the contract

enters its final week of trading, all

eyes will be on how weather forecasts

look to start the month of February to

see where the contract ultimately

expires.

NYMEX FORWARD

CURVES

NYMEX forward natural gas prices

remain in a condition of

backwardation. Bal Cal 22 prices are

currently trading at a 41-cent

premium to Cal 23 prices and a 68-

cent premium to Cal 24 prices. The

spreads have increased slightly as

Bal Cal 22 prices have had a recent

uptick in prices over the course of the

last two weeks due to the arrival of

some sustainable cold weather.

However, the price spreads in the

deferred years of 23 and 24 could

tighten if the market starts to see

these outer years look tighter from a

supply/demand standpoint. Natural

gas storage levels will play an

important role in these spreads. If the

market feels that storage levels could

be well below normal for next heating

season, expect tightening to occur.

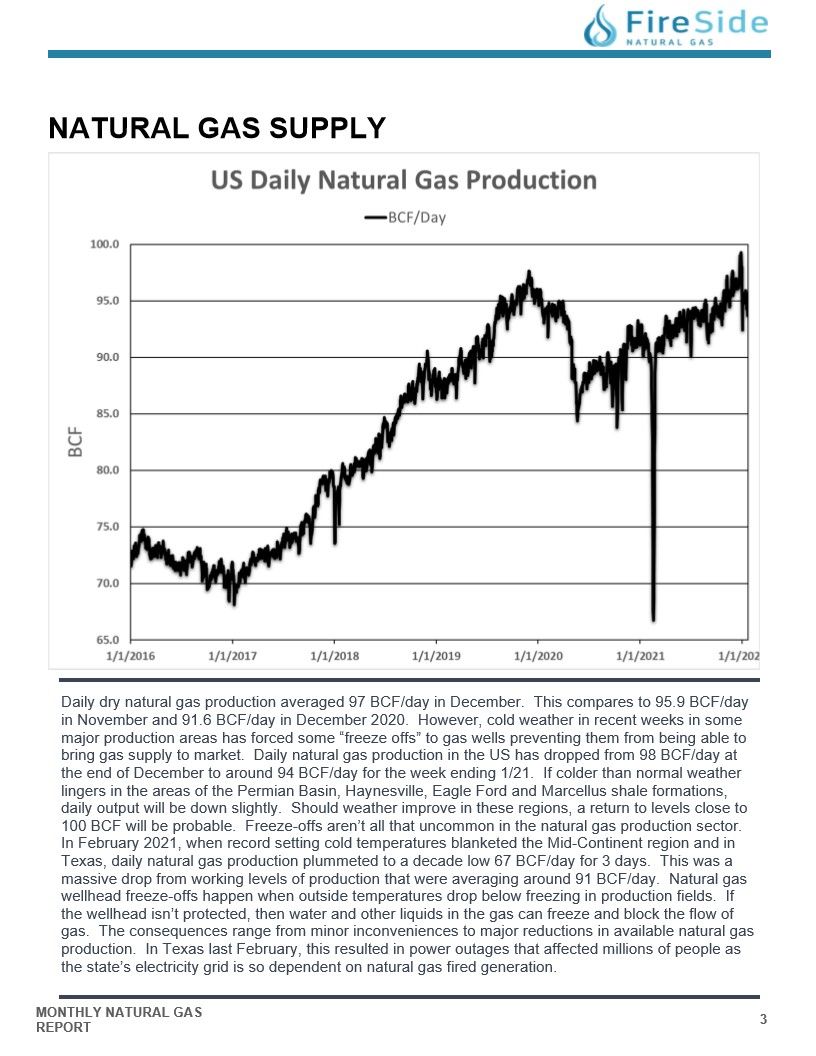

NATURAL GAS SUPPLY - US PRODUCTION

Daily dry natural gas production averaged 97 BCF/day in December. This compares to 95.9 BCF/day

in November and 91.6 BCF/day in December 2020. However, cold weather in recent weeks in some

major production areas has forced some "freeze offs" to gas wells preventing them from being able to

bring gas supply to market. Daily natural gas production in the US has dropped from 98 BCF/day at

the end of December to around 94 BCF/day for the week ending 1/21. If colder than normal weather

lingers in the areas of the Permian Basin, Haynesville, Eagle Ford and Marcellus shale formations,

daily output will be down slightly. Should weather improve in these regions, a return to levels close to

100 BCF will be probable. Freeze-offs aren't all that uncommon in the natural gas production sector.

In February 2021, when record setting cold temperatures blanketed the Mid-Continent region and in

Texas, daily natural gas production plummeted to a decade low 67 BCF/day for 3 days. This was a

massive drop from working levels of production that were averaging around 91 BCF/day. Natural gas

wellhead freeze-offs happen when outside temperatures drop below freezing in production fields. If

the wellhead isn't protected, then water and other liquids in the gas can freeze and block the flow of

gas. The consequences range from minor inconveniences to major reductions in available natural gas

production. In Texas last February, this resulted in power outages that affected millions of people as

the state's electricity grid is so dependent on natural gas fired generation.

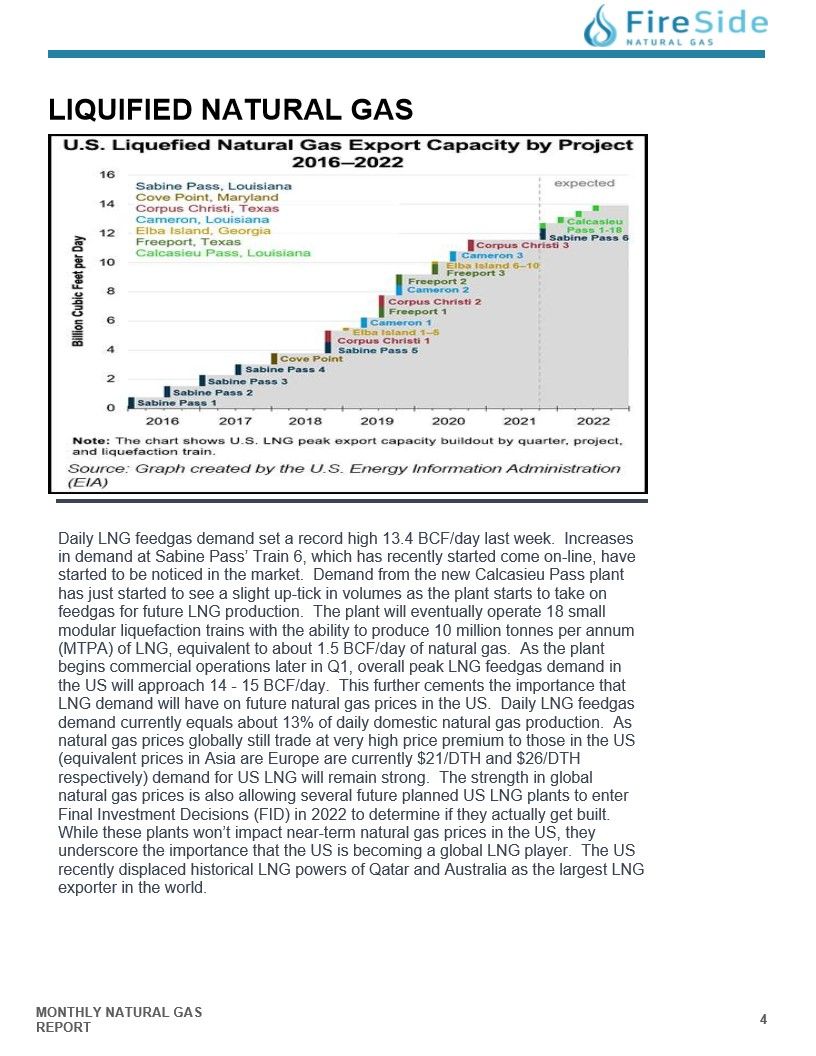

LIQUIFIED NATURAL GAS

Daily LNG feedgas demand set a record high 13.4 BCF/day last week. Increases

in demand at Sabine Pass' Train 6, which has recently started come on-line, have

started to be noticed in the market. Demand from the new Calcasieu Pass plant

has just started to see a slight up-tick in volumes as the plant starts to take on

feedgas for future LNG production. The plant will eventually operate 18 small

modular liquefaction trains with the ability to produce 10 million tonnes per annum

(MTPA) of LNG, equivalent to about 1.5 BCF/day of natural gas. As the plant

begins commercial operations later in Q1, overall peak LNG feedgas demand in

the US will approach 14 - 15 BCF/day. This further cements the importance that

LNG demand will have on future natural gas prices in the US. Daily LNG feedgas

demand currently equals about 13% of daily domestic natural gas production. As

natural gas prices globally still trade at very high price premium to those in the US

(equivalent prices in Asia are Europe are currently $21/DTH and $26/DTH

respectively) demand for US LNG will remain strong. The strength in global

natural gas prices is also allowing several future planned US LNG plants to enter

Final Investment Decisions (FID) in 2022 to determine if they actually get built.

While these plants won't impact near-term natural gas prices in the US, they

underscore the importance that the US is becoming a global LNG player. The US

recently displaced historical LNG powers of Qatar and Australia as the largest LNG

exporter in the world.

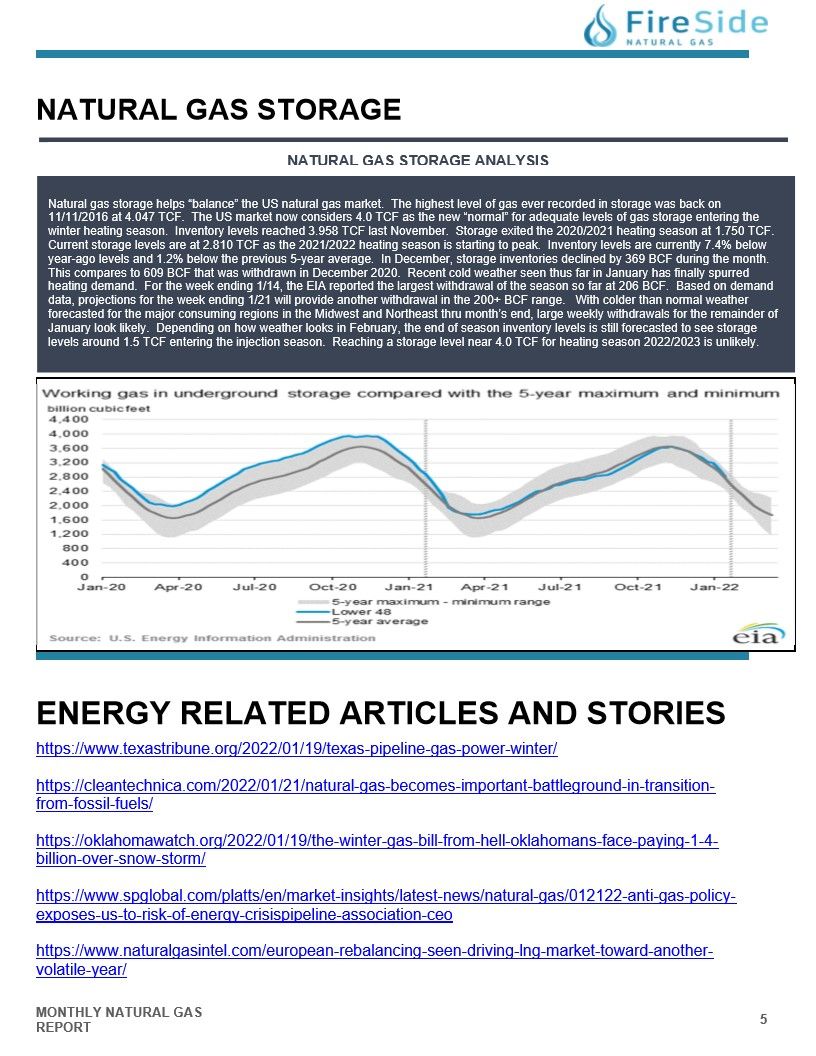

NATURAL GAS STORAGE - STORAGE ANALYSIS

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on

11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas storage entering the

winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating season at 1.750 TCF.

Current storage levels are at 2.810 TCF as the 2021/2022 heating season is starting to peak. Inventory levels are currently 7.4% below

year-ago levels and 1.2% below the previous 5-year average. In December, storage inventories declined by 369 BCF during the month.

This compares to 609 BCF that was withdrawn in December 2020. Recent cold weather seen thus far in January has finally spurred

heating demand. For the week ending 1/14, the EIA reported the largest withdrawal of the season so far at 206 BCF. Based on demand

data, projections for the week ending 1/21 will provide another withdrawal in the 200+ BCF range. With colder than normal weather

forecasted for the major consuming regions in the Midwest and Northeast thru month's end, large weekly withdrawals for the remainder of

January look likely. Depending on how weather looks in February, the end of season inventory levels is still forecasted to see storage

levels around 1.5 TCF entering the injection season. Reaching a storage level near 4.0 TCF for heating season 2022/2023 is unlikely.

Energy Related Articles and Stories

https://www.texastribune.org/2022/01/19/texas-pipeline-gas-power-winter/