The Weekly Natural Gas Market Newsletter February 14, 2022

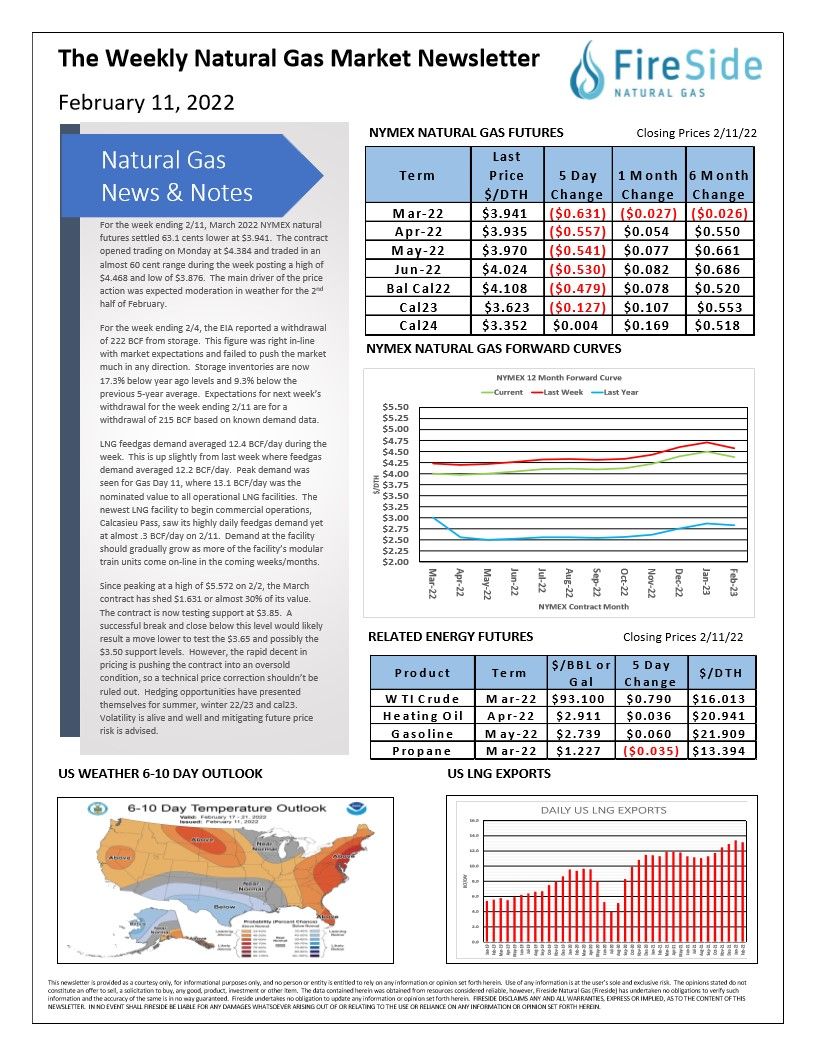

For the week ending 2/11, March 2022 NYMEX natural futures settled 63.1 cents lower at $3.941. The contract opened trading on Monday at $4.384 and traded in an almost 60 cent range during the week posting a high of $4.468 and low of $3.876. The main driver of the price action was expected moderation in weather for the 2nd half of February.

For the week ending 2/4, the EIA reported a withdrawal of 222 BCF from storage. This figure was right in-line with market expectations and failed to push the market much in any direction. Storage inventories are now 17.3% below year ago levels and 9.3% below the previous 5-year average. Expectations for next week's withdrawal for the week ending 2/11 are for a withdrawal of 215 BCF based on known demand data.

LNG feedgas demand averaged 12.4 BCF/day during the week. This is up slightly from last week where feedgas demand averaged 12.2 BCF/day. Peak demand was seen for Gas Day 11, where 13.1 BCF/day was the nominated value to all operational LNG facilities. The newest LNG facility to begin commercial operations, Calcasieu Pass, saw its highly daily feedgas demand yet at almost .3 BCF/day on 2/11. Demand at the facility should gradually grow as more of the facility's modular train units come on-line in the coming weeks/months.

Since peaking at a high of $5.572 on 2/2, the March

contract has shed $1.631 or almost 30% of its value.

The contract is now testing support at $3.85. A

successful break and close below this level would likely

result a move lower to test the $3.65 and possibly the

$3.50 support levels. However, the rapid decent in

pricing is pushing the contract into an oversold

condition, so a technical price correction shouldn't be

ruled out. Hedging opportunities have presented

themselves for summer, winter 22/23 and cal23.

Volatility is alive and well and mitigating future price

risk is advised.