The Monthly Natural Gas Market Newsletter - December 2021

FireSide Natural Gas Monthly Report - December 2021

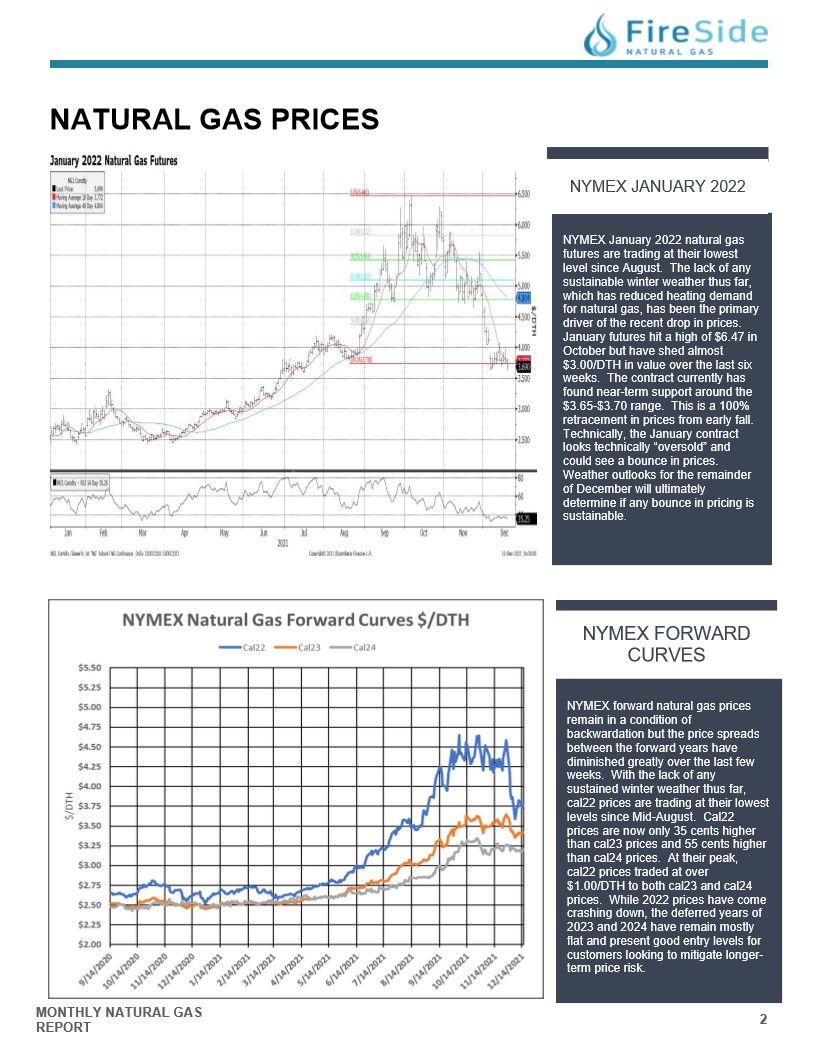

Natural Gas Prices

NYMEX January 2022

NYMEX January 2022 natural gas

futures are trading at their lowest

level since August. The lack of any

sustainable winter weather thus far,

which has reduced heating demand

for natural gas, has been the primary

driver of the recent drop in prices.

January futures hit a high of $6.47 in

October but have shed almost

$3.00/DTH in value over the last six

weeks. The contract currently has

found near-term support around the

$3.65-$3.70 range. This is a 100%

retracement in prices from early fall.

Technically, the January contract

looks technically "oversold" and

could see a bounce in prices.

Weather outlooks for the remainder

of December will ultimately

determine if any bounce in pricing is

sustainable.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of

backwardation but the price spreads

between the forward years have

diminished greatly over the last few

weeks. With the lack of any

sustained winter weather thus far,

cal22 prices are trading at their lowest

levels since Mid-August. Cal22

prices are now only 35 cents higher

than cal23 prices and 55 cents higher

than cal24 prices. At their peak,

cal22 prices traded at over

$1.00/DTH to both cal23 and cal24

prices. While 2022 prices have come

crashing down, the deferred years of

2023 and 2024 have remain mostly

flat and present good entry levels for

customers looking to mitigate longer-term price risk.

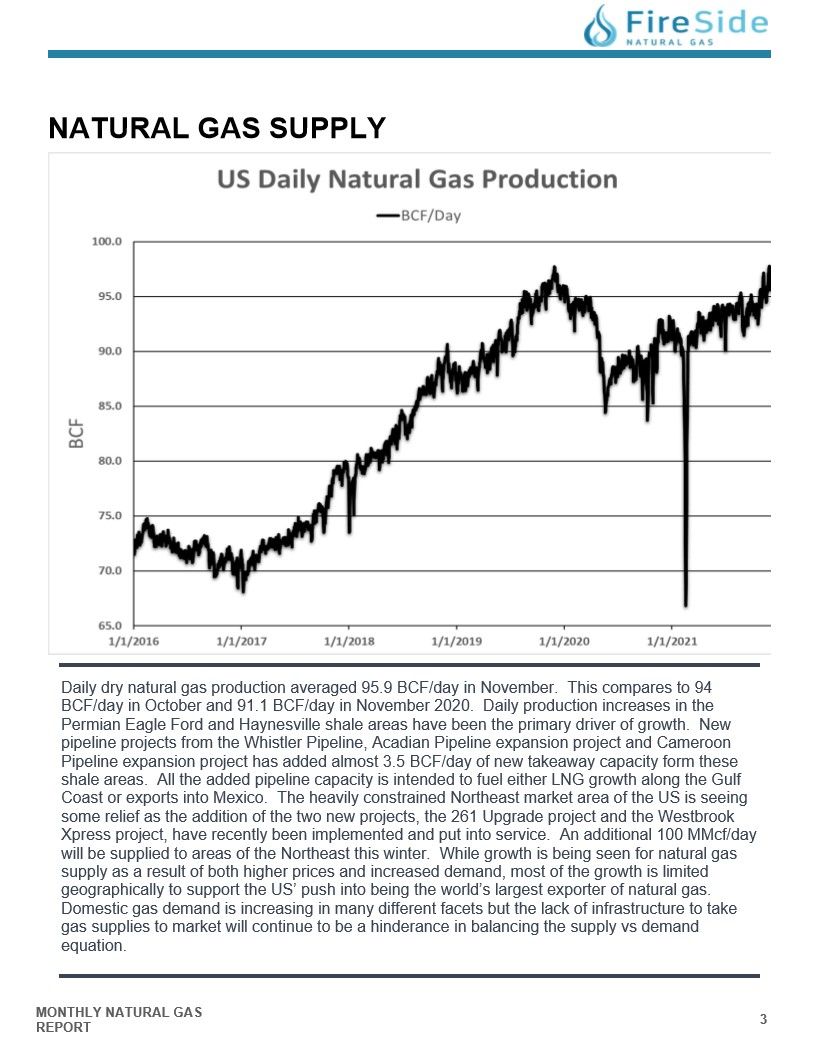

Natural Gas Supply - Daily US Natural Gas Production

Daily dry natural gas production averaged 95.9 BCF/day in November. This compares to 94

BCF/day in October and 91.1 BCF/day in November 2020. Daily production increases in the

Permian Eagle Ford and Haynesville shale areas have been the primary driver of growth. New

pipeline projects from the Whistler Pipeline, Acadian Pipeline expansion project and Cameroon

Pipeline expansion project has added almost 3.5 BCF/day of new takeaway capacity form these

shale areas. All the added pipeline capacity is intended to fuel either LNG growth along the Gulf

Coast or exports into Mexico. The heavily constrained Northeast market area of the US is seeing

some relief as the addition of the two new projects, the 261 Upgrade project and the Westbrook

Xpress project, have recently been implemented and put into service. An additional 100 MMcf/day

will be supplied to areas of the Northeast this winter. While growth is being seen for natural gas

supply as a result of both higher prices and increased demand, most of the growth is limited

geographically to support the US' push into being the world's largest exporter of natural gas.

Domestic gas demand is increasing in many different facets but the lack of infrastructure to take

gas supplies to market will continue to be a hinderance in balancing the supply vs demand

equation.

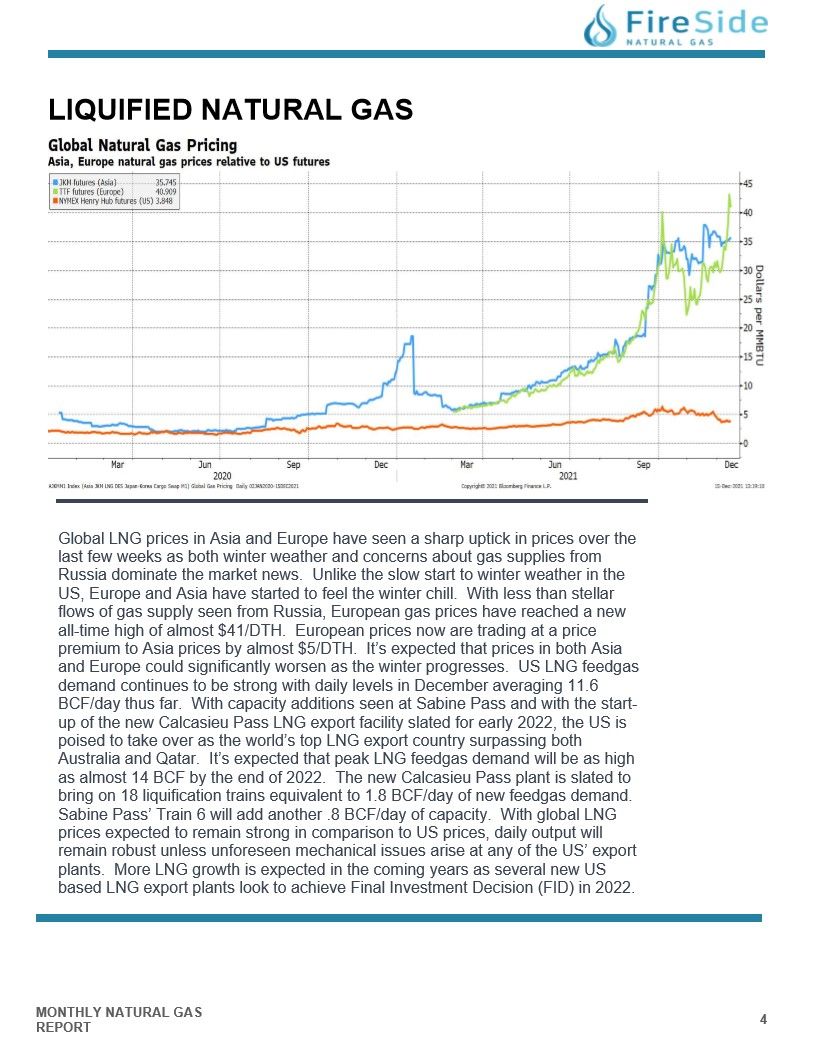

Liquified Natural Gas - Global Natural Gas Pricing

Global LNG prices in Asia and Europe have seen a sharp uptick in prices over the

last few weeks as both winter weather and concerns about gas supplies from

Russia dominate the market news. Unlike the slow start to winter weather in the

US, Europe and Asia have started to feel the winter chill. With less than stellar

flows of gas supply seen from Russia, European gas prices have reached a new

all-time high of almost $41/DTH. European prices now are trading at a price

premium to Asia prices by almost $5/DTH. It's expected that prices in both Asia

and Europe could significantly worsen as the winter progresses. US LNG feedgas

demand continues to be strong with daily levels in December averaging 11.6

BCF/day thus far. With capacity additions seen at Sabine Pass and with the startup of the new Calcasieu Pass LNG export facility slated for early 2022, the US is

poised to take over as the world's top LNG export country surpassing both

Australia and Qatar. It's expected that peak LNG feedgas demand will be as high

as almost 14 BCF by the end of 2022. The new Calcasieu Pass plant is slated to

bring on 18 liquification trains equivalent to 1.8 BCF/day of new feedgas demand.

Sabine Pass' Train 6 will add another .8 BCF/day of capacity. With global LNG

prices expected to remain strong in comparison to US prices, daily output will

remain robust unless unforeseen mechanical issues arise at any of the US' export

plants. More LNG growth is expected in the coming years as several new US

based LNG export plants look to achieve Final Investment Decision (FID) in 2022.

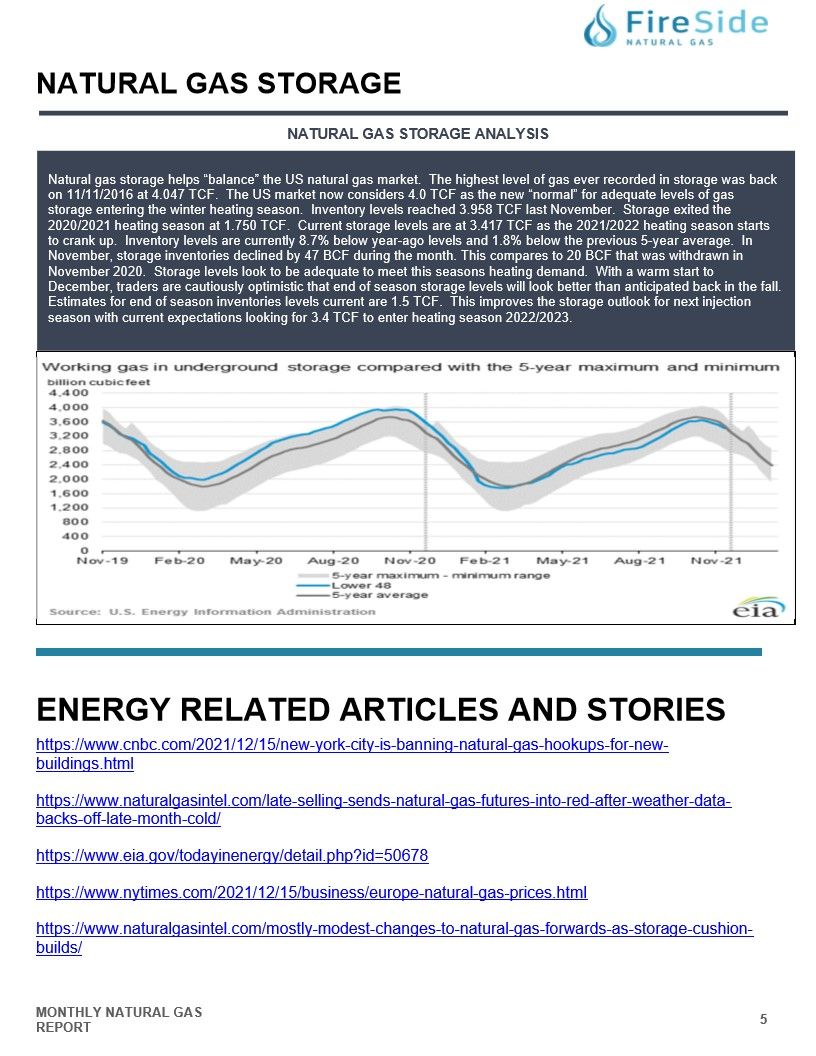

Natural Gas Storage Analysis

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back

on 11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas

storage entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the

2020/2021 heating season at 1.750 TCF. Current storage levels are at 3.417 TCF as the 2021/2022 heating season starts

to crank up. Inventory levels are currently 8.7% below year-ago levels and 1.8% below the previous 5-year average. In

November, storage inventories declined by 47 BCF during the month. This compares to 20 BCF that was withdrawn in

November 2020. Storage levels look to be adequate to meet this seasons heating demand. With a warm start to

December, traders are cautiously optimistic that end of season storage levels will look better than anticipated back in the fall.

Estimates for end of season inventories levels current are 1.5 TCF. This improves the storage outlook for next injection

season with current expectations looking for 3.4 TCF to enter heating season 2022/2023.

https://www.cnbc.com/2021/12/15/new-york-city-is-banning-natural-gas-hookups-for-newbuildings.html

https://www.eia.gov/todayinenergy/detail.php?id=50678

https://www.nytimes.com/2021/12/15/business/europe-natural-gas-prices.html