The Weekly Natural Gas Market Newsletter December 13, 2021

January 2022 NYMEX natural gas futures settled at $3.925 on Friday. The contract ended the week down 20.7 cents as the lack of any sustained winter weather continues to pressure natural gas prices lower. Unlike the previous trading week that saw natural gas prices plunge 20%, trading this week kept the January contract in a much narrower 30 cent trading range. The contract gapped down in overnight trade Sunday to a low of $3.63 but ultimately found bargain seeking buyers amidst the lowest prices seen since late August.

For the week ending 12/3, the EIA reported a withdrawal of 59 BCF. The withdrawal was slightly larger than most market estimates but failed to move the January contract in any meaningful direction. Inventories now stand at 9.2% below last year's level and 2.5% below the previous 5-year average. Storage inventory levels look much healthier than they did just a few weeks ago as warmer weather has prevented any major withdrawals from storage thus far this heating season.

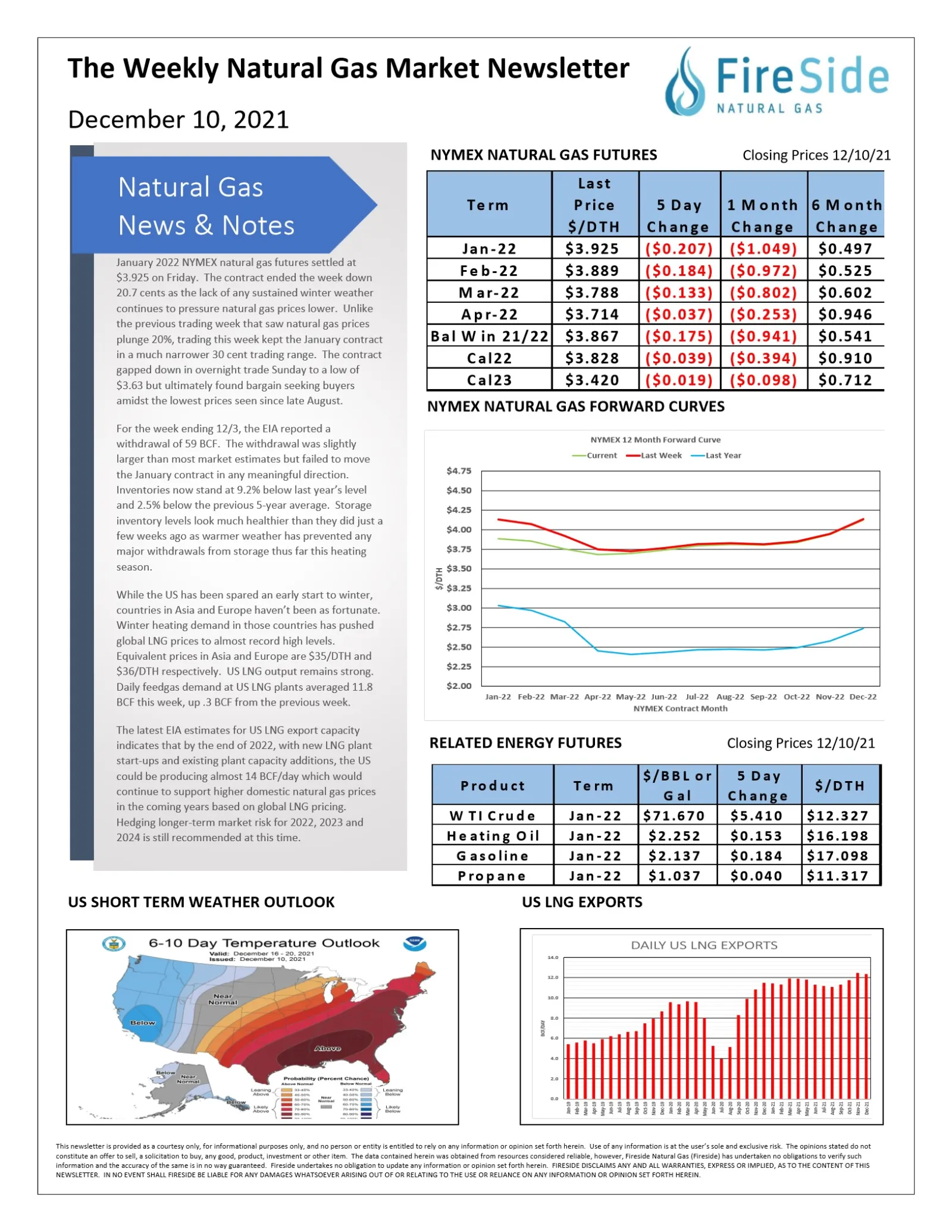

While the US has been spared an early start to winter, countries in Asia and Europe haven't been as fortunate. Winter heating demand in those countries has pushed global LNG prices to almost record high levels. Equivalent prices in Asia and Europe are $35/DTH and $36/DTH respectively. US LNG output remains strong. Daily feedgas demand at US LNG plants averaged 11.8 BCF this week, up .3 BCF from the previous week.

The latest EIA estimates for US LNG export capacity

indicates that by the end of 2022, with new LNG plant

start-ups and existing plant capacity additions, the US

could be producing almost 14 BCF/day which would

continue to support higher domestic natural gas prices

in the coming years based on global LNG pricing.

Hedging longer-term market risk for 2022, 2023 and

2024 is still recommended at this time