The Monthly Natural Gas Market Newsletter - April 2022

FireSide Natural Gas Monthly Report - April 2022

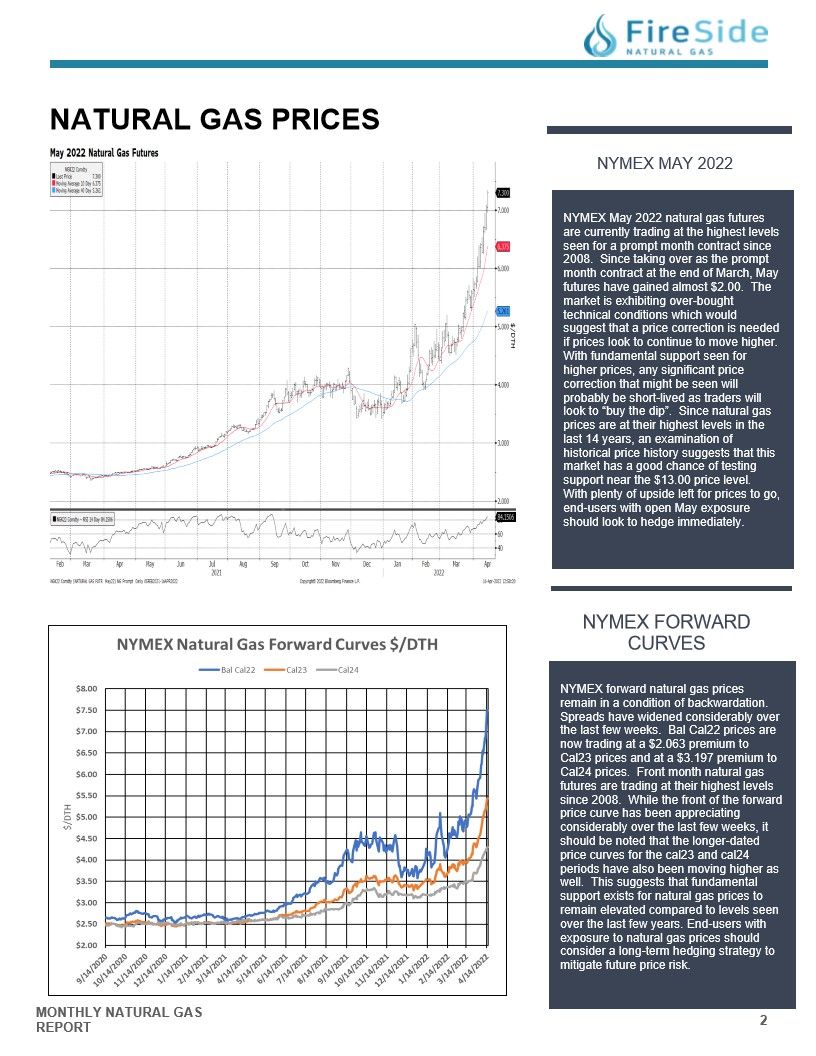

Natural Gas Prices

NYMEX MAY 2022

NYMEX May 2022 natural gas futures

are currently trading at the highest levels

seen for a prompt month contract since

2008. Since taking over as the prompt

month contract at the end of March, May

futures have gained almost $2.00. The

market is exhibiting over-bought

technical conditions which would

suggest that a price correction is needed

if prices look to continue to move higher.

With fundamental support seen for

higher prices, any significant price

correction that might be seen will

probably be short-lived as traders will

look to "buy the dip". Since natural gas

prices are at their highest levels in the

last 14 years, an examination of

historical price history suggests that this

market has a good chance of testing

support near the $13.00 price level.

With plenty of upside left for prices to go,

end-users with open May exposure

should look to hedge immediately.

NYMEX FORWARD CURVES

NYMEX forward natural gas prices

remain in a condition of backwardation.

Spreads have widened considerably over

the last few weeks. Bal Cal22 prices are

now trading at a $2.063 premium to

Cal23 prices and at a $3.197 premium to

Cal24 prices. Front month natural gas

futures are trading at their highest levels

since 2008. While the front of the forward

price curve has been appreciating

considerably over the last few weeks, it

should be noted that the longer-dated

price curves for the cal23 and cal24

periods have also been moving higher as

well. This suggests that fundamental

support exists for natural gas prices to

remain elevated compared to levels seen

over the last few years. End-users with

exposure to natural gas prices should

consider a long-term hedging strategy to

mitigate future price risk.

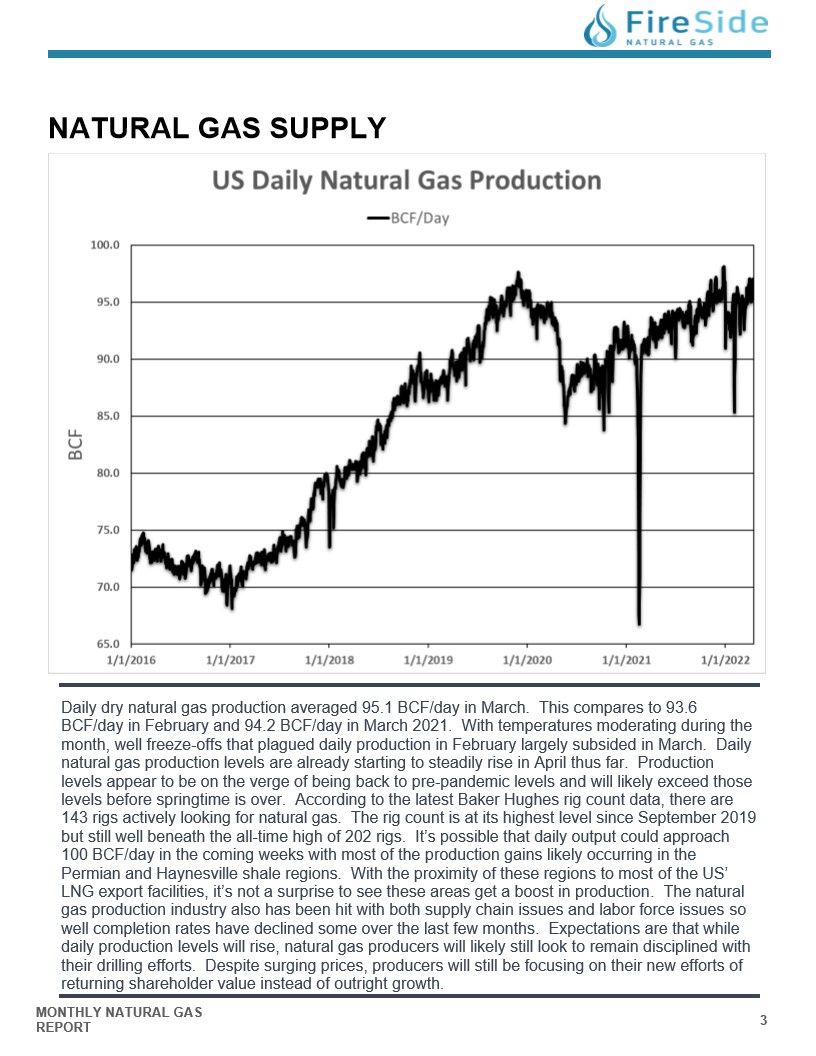

Natural Gas Supply - US Daily Natural Gas Production

Daily dry natural gas production averaged 95.1 BCF/day in March. This compares to 93.6

BCF/day in February and 94.2 BCF/day in March 2021. With temperatures moderating during the

month, well freeze-offs that plagued daily production in February largely subsided in March. Daily

natural gas production levels are already starting to steadily rise in April thus far. Production

levels appear to be on the verge of being back to pre-pandemic levels and will likely exceed those

levels before springtime is over. According to the latest Baker Hughes rig count data, there are

143 rigs actively looking for natural gas. The rig count is at its highest level since September 2019

but still well beneath the all-time high of 202 rigs. It's possible that daily output could approach

100 BCF/day in the coming weeks with most of the production gains likely occurring in the

Permian and Haynesville shale regions. With the proximity of these regions to most of the US'

LNG export facilities, it's not a surprise to see these areas get a boost in production. The natural

gas production industry also has been hit with both supply chain issues and labor force issues so

well completion rates have declined some over the last few months. Expectations are that while

daily production levels will rise, natural gas producers will likely still look to remain disciplined with

their drilling efforts. Despite surging prices, producers will still be focusing on their new efforts of

returning shareholder value instead of outright growth.

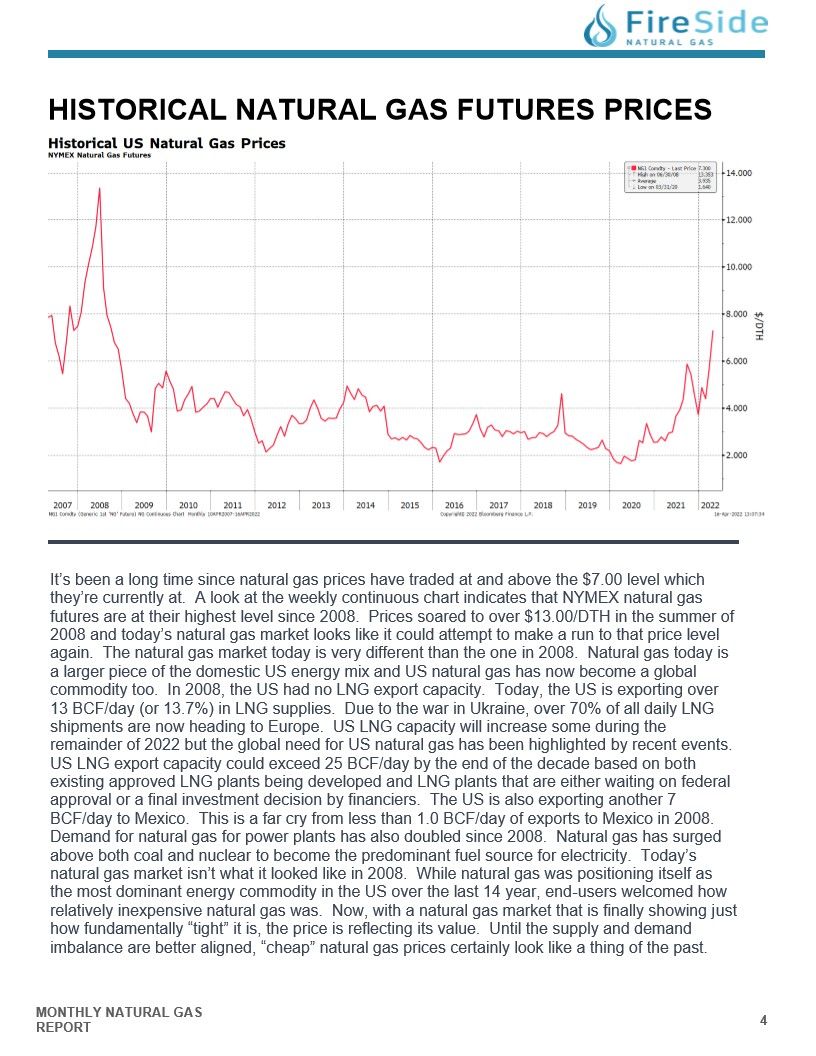

Historical Natural Gas Futures Prices

It's been a long time since natural gas prices have traded at and above the $7.00 level which

they're currently at. A look at the weekly continuous chart indicates that NYMEX natural gas

futures are at their highest level since 2008. Prices soared to over $13.00/DTH in the summer of

2008 and today's natural gas market looks like it could attempt to make a run to that price level

again. The natural gas market today is very different than the one in 2008. Natural gas today is

a larger piece of the domestic US energy mix and US natural gas has now become a global

commodity too. In 2008, the US had no LNG export capacity. Today, the US is exporting over

13 BCF/day (or 13.7%) in LNG supplies. Due to the war in Ukraine, over 70% of all daily LNG

shipments are now heading to Europe. US LNG capacity will increase some during the

remainder of 2022 but the global need for US natural gas has been highlighted by recent events.

US LNG export capacity could exceed 25 BCF/day by the end of the decade based on both

existing approved LNG plants being developed and LNG plants that are either waiting on federal

approval or a final investment decision by financiers. The US is also exporting another 7

BCF/day to Mexico. This is a far cry from less than 1.0 BCF/day of exports to Mexico in 2008.

Demand for natural gas for power plants has also doubled since 2008. Natural gas has surged

above both coal and nuclear to become the predominant fuel source for electricity. Today's

natural gas market isn't what it looked like in 2008. While natural gas was positioning itself as

the most dominant energy commodity in the US over the last 14 year, end-users welcomed how

relatively inexpensive natural gas was. Now, with a natural gas market that is finally showing just

how fundamentally "tight" it is, the price is reflecting its value. Until the supply and demand

imbalance are better aligned, "cheap" natural gas prices certainly look like a thing of the past.

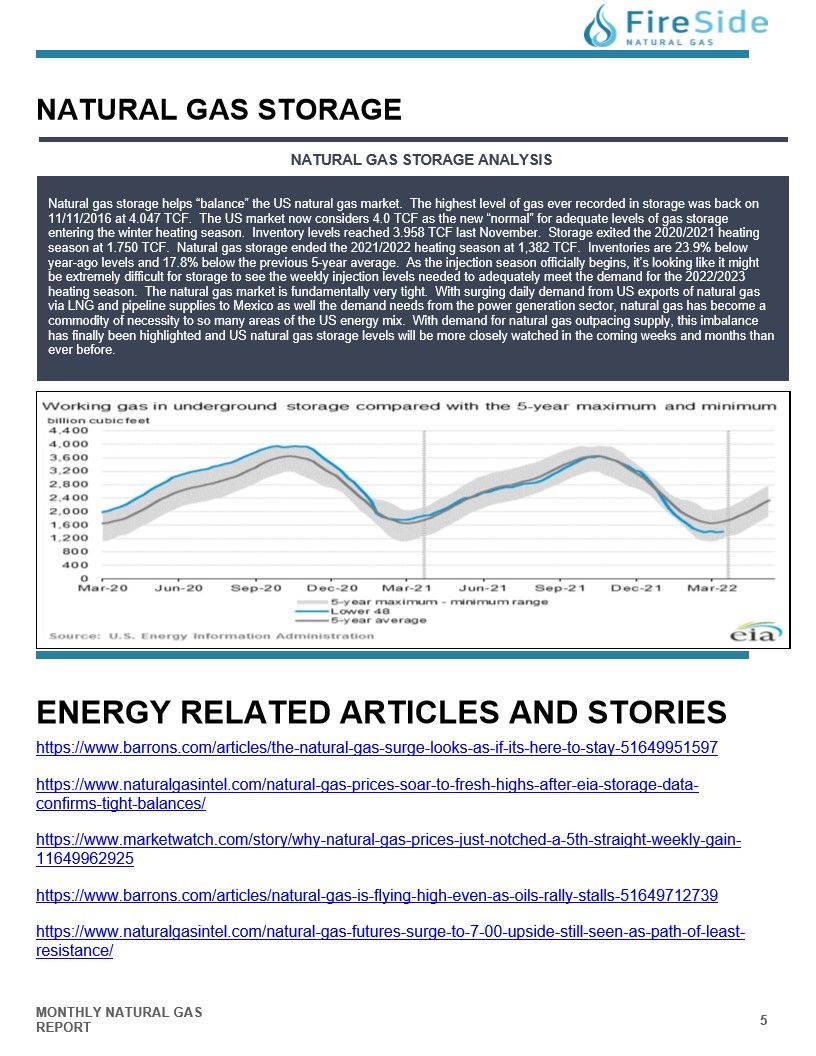

Natural Gas Storage - Natural Gas Storage Analysis

Natural gas storage helps "balance" the US natural gas market. The highest level of gas ever recorded in storage was back on

11/11/2016 at 4.047 TCF. The US market now considers 4.0 TCF as the new "normal" for adequate levels of gas storage

entering the winter heating season. Inventory levels reached 3.958 TCF last November. Storage exited the 2020/2021 heating

season at 1.750 TCF. Natural gas storage ended the 2021/2022 heating season at 1,382 TCF. Inventories are 23.9% below

year-ago levels and 17.8% below the previous 5-year average. As the injection season officially begins, it's looking like it might

be extremely difficult for storage to see the weekly injection levels needed to adequately meet the demand for the 2022/2023

heating season. The natural gas market is fundamentally very tight. With surging daily demand from US exports of natural gas

via LNG and pipeline supplies to Mexico as well the demand needs from the power generation sector, natural gas has become a

commodity of necessity to so many areas of the US energy mix. With demand for natural gas outpacing supply, this imbalance

has finally been highlighted and US natural gas storage levels will be more closely watched in the coming weeks and months than

ever before.

Energy Related Articles and Stories

https://www.barrons.com/articles/the-natural-gas-surge-looks-as-if-its-here-to-stay-51649951597

https://www.barrons.com/articles/natural-gas-is-flying-high-even-as-oils-rally-stalls-51649712739